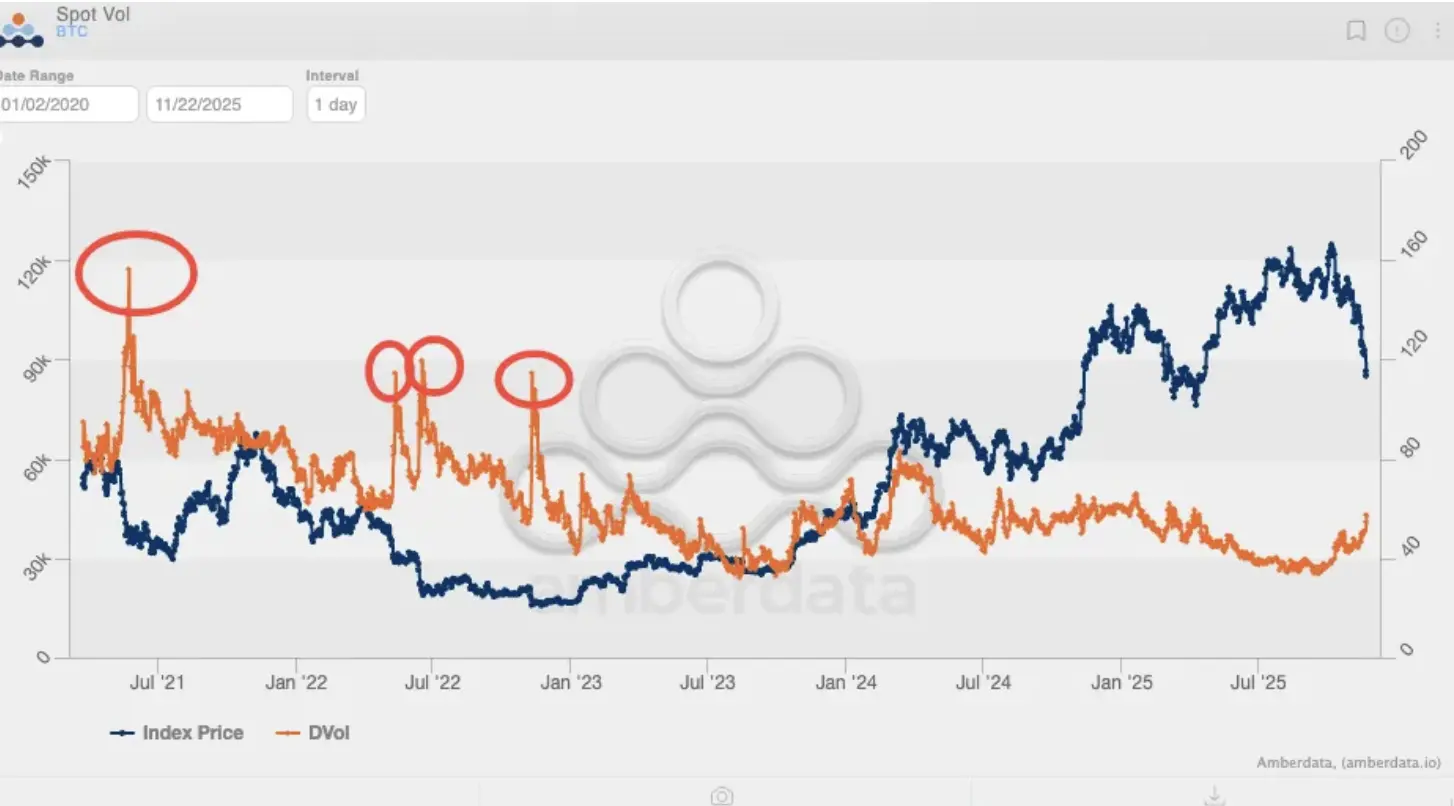

In the past two months, Bitcoin’s price volatility has risen sharply, signaling that price trends may be returning to an options-driven mode, which could trigger significant two-way swings in the market. According to Jeff Park, market analyst and advisor at investment firm Bitwise, since the approval of Bitcoin ETFs in the US, Bitcoin’s implied volatility had never exceeded 80%. However, as of this writing, Bitcoin’s volatility is slowly climbing back toward around 60.

Volatility Rebounds to 60, Signaling a Return to Options Dominance

(Source: Amberdata)

Charts shared by Park show that historically, before Bitcoin exchange-traded funds (ETFs) were approved for trading in the US market in 2024, Bitcoin prices experienced significant swings. After ETF approval, Bitcoin’s implied volatility was suppressed at relatively low levels, never exceeding 80%. This suppression effect is believed to result from institutional investors engaging in passive allocation through ETFs, with large, stable capital inflows smoothing out price fluctuations.

However, recent data from the past two months indicate that this calm may be coming to an end. Bitcoin’s volatility is slowly rebounding to around 60. Although it has not yet reached pre-ETF levels above 80%, the trend itself is highly significant. Rising volatility is usually accompanied by increased market uncertainty and more active trading, creating the right conditions for a vibrant options market.

Implied volatility is derived from options prices and reflects the market’s expectations for future price swings. When implied volatility rises, it means options buyers are willing to pay higher premiums for protection or speculation. This increased demand, in turn, affects the spot market, as options sellers must hedge their positions in the spot market. This dynamic interaction is known as the “options-driven” model.

Park stated, “Ultimately, what really pushes Bitcoin to new highs is options positioning, not just spot trading. For the first time in nearly two years, surface volatility may be showing early signs that Bitcoin prices could once again be driven by options.” This perspective challenges the mainstream narrative that ETFs have already transformed Bitcoin into a more mature and stable asset class.

On a technical level, the options-driven price model is self-reinforcing. When the market expects volatility to rise, options buying increases, and sellers must hedge their risks by building positions in the spot market. If demand for call options increases, sellers need to buy spot to hedge, pushing the price higher; the reverse is also true. This mechanism creates an acceleration effect during price trends, resulting in sharp two-way swings.

Lessons from the Options-Driven Bull Market of 2021

Park pointed out that Bitcoin’s explosive price action in January 2021 kicked off that year’s bull market, with prices soaring to new all-time highs and reaching a cyclical peak of $69,000 in November—the last time a major rally was options-driven. Reviewing that history is valuable for understanding the current market.

In January 2021, Bitcoin’s price quickly jumped from around $30,000 to $40,000 and continued to climb over the following months. This rally was characterized by extremely high volatility, with daily swings often exceeding 10%, and was accompanied by unusually active options trading. At the time, data showed that Bitcoin options open interest and trading volumes both hit record highs, with implied volatility staying above 80% for extended periods and even exceeding 120% at its peak.

The active options market provided strong momentum for spot prices. Many institutional and retail investors engaged in leveraged speculation by buying call options, forcing option sellers to continuously buy Bitcoin in the spot market to hedge their risks. This “Gamma Squeeze” effect was especially evident when Bitcoin broke through key resistance levels; each breakout was accompanied by passive buying from options sellers, further driving up prices.

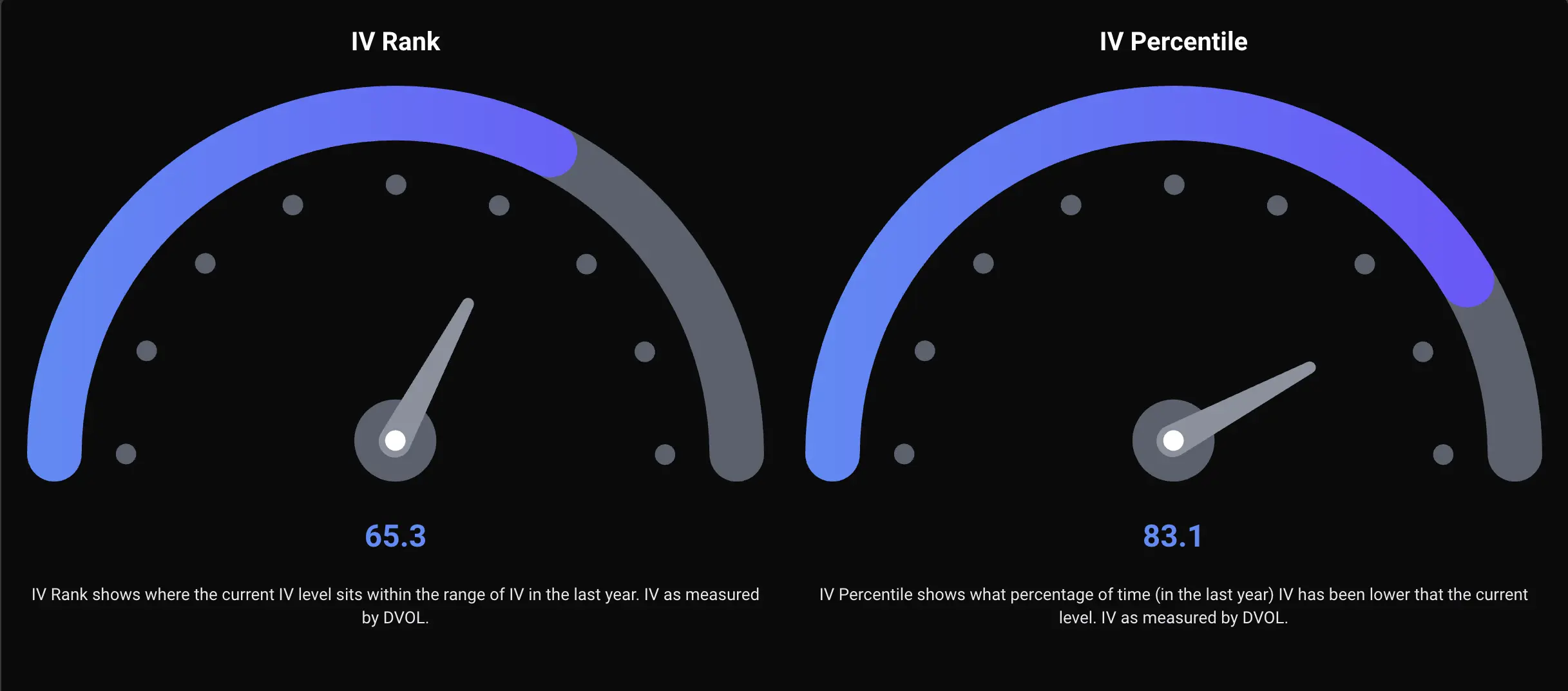

The similarities between the current market and January 2021 include the rebound in volatility and increased activity in the options market. Data from Deribit shows that the rank and percentile of Bitcoin options’ implied volatility are rising, indicating that current volatility levels have rebounded from historical lows. If this trend continues, the market could see a return to the kind of options-driven, high-volatility swings seen in 2021.

Three Key Features of the 2021 Options-Driven Bull Market

Implied volatility consistently above 80%: Provided rich premiums for the options market, attracting significant speculative capital

Significant Gamma Squeeze Effect: Options sellers were forced to hedge in the spot market, accelerating price increases

Positive Feedback Loop Between Volatility and Price: Price rises → volatility increases → options demand rises → more spot hedging buys → further price increases

However, it’s important to note that options-driven markets are two-sided. After reaching the $69,000 peak in November 2021, Bitcoin immediately entered a prolonged bear market, dropping to $15,500 in November 2022. This decline was also accompanied by high volatility and active options trading, just in the opposite direction. When demand for put options increases, sellers need to sell spot to hedge, accelerating price declines.

Is the ETF Calm Ending? Reassessing Institutional Influence

(Source: Deribit)

This analysis counters the theory that ETFs and institutional investors have permanently dampened Bitcoin’s price volatility and shifted the market structure to reflect a more mature asset class, supported by passive inflows into investment vehicles. This rebuttal has important market implications, as it means Bitcoin remains a high-risk, high-volatility speculative asset, not yet a fully matured store of value.

After Bitcoin ETFs were approved in January 2024, it was widely expected that institutional inflows would make Bitcoin’s price more stable. Indeed, in the months following ETF launches, Bitcoin’s volatility dropped markedly, with narrower intraday swings and smoother price action. This was interpreted as Bitcoin “growing up,” transitioning from a purely speculative asset to a legitimate option for institutional allocation.

However, on Thursday, Bitcoin’s price plunged below $85,000, sparking concerns about further declines in the coming weeks and the potential start of the next Bitcoin bear market. This crash broke the ETF-induced calm, with volatility surging dramatically. Analysts have put forward several theories for the drop, including the liquidation of highly leveraged derivatives positions, long-term holders cashing out, and macroeconomic pressures.

The Binance CEO stated that Bitcoin’s high volatility is consistent with the volatility levels of all asset classes. This viewpoint suggests that the current rise in volatility may not be unique to Bitcoin, but rather a reflection of broader market uncertainty. The deteriorating global macroeconomic environment, rising geopolitical risks, and uncertainty in monetary policy could all cause volatility to increase across all risk assets.

Short-Term Correction or Start of a Long Bear Market? Analysts Divided

According to analysts at CEX, Bitcoin’s continued decline is due to short-term factors, indicating that the market is undergoing “tactical rebalancing” rather than institutional outflows or a lack of demand. This view is relatively optimistic, seeing current volatility and declines as a healthy correction within a bull market, not a trend reversal.

Analysts said this would not affect Bitcoin’s long-term fundamentals, price growth, or institutional adoption trend. Supporting evidence includes: ETF inflows remain positive overall despite fluctuations, the number of on-chain long-term holders continues to increase, and institutional adoption is progressing steadily. From this perspective, rising volatility is simply the market seeking a new equilibrium, and once short-term factors subside, the upward trend will continue.

However, if volatility continues to rise and the market enters an options-driven mode, Bitcoin could face violent two-way swings. This means prices could surge or plunge rapidly, depending on the direction of options market demand and changes in the macro environment.