The Solana DEX ecosystem in early 2026 has undergone a clear and accelerating bifurcation, splitting into two fundamentally different worlds with opposing paths to survival and dominance:

(Sources:Blockwork)

- Active market-making AMMs now command the majority of short-tail, high-liquidity volume (SOL–USDC, SOL–USDT, major stable pairs, tokenized RWAs, blue-chip assets).

- Passive AMMs have been almost entirely relegated to long-tail assets, newly launched tokens, and issuance-dependent flow.

The winning strategies for each camp have become polar opposites, and both are increasingly defined by vertical integration—but in completely different directions. This analyst insight breaks down the current state of the Solana DEX market, the structural forces driving the split, the leading protocols in each category, valuation considerations, and the outlook for the year ahead.

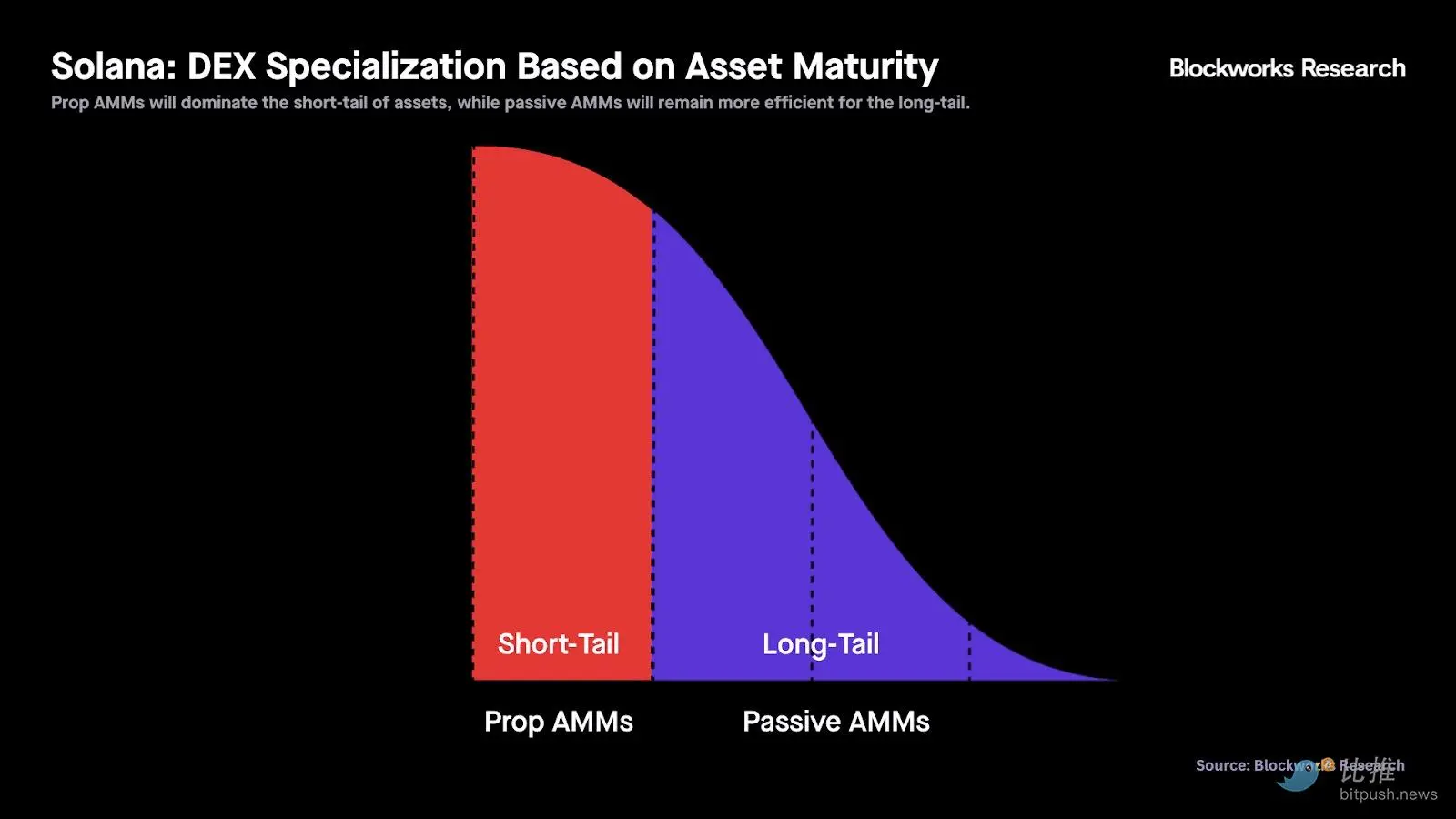

Professionalization & Polarization: Short-Tail vs Long-Tail Dominance

Active AMMs have captured over 50% of all Solana spot trading volume, almost entirely concentrated in deep, oracle-fed pairs where execution quality is paramount. Passive AMMs (classic Raydium, Orca, Meteora pools) still provide the majority of day-one liquidity for new tokens and long-tail assets, but their share of high-liquidity flow has collapsed dramatically.

Most telling statistic: none of the newer-generation passive AMMs (PumpSwap, Futarchy AMM, Jupiter DTF pools) even bother creating pools for SOL–USDC or SOL–USDT. They recognize they cannot compete on price, latency, or reliability in the short tail.

- Active AMM Share: >50% of spot volume, hyper-concentrated in majors.

- Passive AMM Role: Day-1 liquidity, long-tail provision, issuance monetization.

- Structural Shift: Short-tail has become a high-frequency execution game; long-tail remains a social/issuance game.

Order Flow Capture: Execution vs Issuance – The Two Paths to Moat

Active AMMs have almost no native front-end traffic. Over 95% of HumidiFi volume arrives via aggregators (Jupiter, DFlow, etc.). Their entire business depends on winning the aggregator routing decision by offering the tightest, fastest, most reliable execution.

(Sources:Blockwork)

This creates relentless competition on:

- Price (markout, slippage)

- Latency (oracle freshness, transaction ordering)

- Reliability (uptime, failed tx rate)

Hence active AMMs are extending downstream—owning bundling, sequencing, private mempools, and execution services (Nozomi is the clearest example).

Passive AMMs, conversely, have lost the execution battle on short-tail pairs. Their only remaining durable path is controlling issuance order flow. The most sustainable passive AMM model in 2026 is one that is vertically integrated as an issuance platform first, with the AMM acting as the monetization layer for graduated or ICO’d tokens.

Typical end-state winners in the passive camp now look like:

- High-velocity meme launchpads → own AMM (Pump → PumpSwap)

- Curated ICO / token-formation platforms → own AMM (MetaDAO → Futarchy AMM, Jupiter DTF → Meteora pools)

HumidiFi Dominance: The Clear Leader in Active Market Making

HumidiFi now controls ~65% of active AMM volume on Solana, with Tessera (~18%) and GoonFi (~7%) as distant followers.

Key structural advantages:

- Temporal Labs engineering team widely regarded as one of Solana’s strongest.

- Vertical integration with Nozomi (execution/landing service) and Harmonic (block builder competing with Jito) creates meaningful latency and ordering edge.

- Co-founder Kevin Pang brings high-frequency trading pedigree from Jump, Paradigm, Symbolic Capital.

- Oracle update instructions optimized to ~47 compute units (down >85% since launch); total tx CU under 500—lowest in class.

Volume is hyper-concentrated: ~98% from SOL–USDC (83%) and SOL–USDT (14%). CEX–DEX arbitrage has flipped on-chain; active AMMs now capture many opportunities atomically, reducing cross-venue risk and rewarding the fastest updater (HumidiFi).

Passive AMMs on SOL–USD Stable Pairs: A Losing Game

Markout analysis (30-second post-trade price movement) shows active AMMs consistently generate positive markouts on SOL–USDC, while passive pools suffer negative markouts—clear evidence of adverse selection.

Passive liquidity providers on SOL-stable pairs are increasingly arbitraged by bots exploiting stale quotes. The inevitable outcome: LP capital flees high-liquidity pairs unless heavily subsidized by emissions (which are unsustainable long-term).

Classic passive AMMs survive only as:

- Backstop liquidity during active AMM withdrawals

- Day-1 liquidity for new tokens

- Monetization layer for issuance platforms

The Death of the Standalone DEX on Solana

The most consequential takeaway for the Solana DEX ecosystem in 2026 is that the standalone, general-purpose passive DEX model is dying.

A pure AMM without either:

- Superior execution (active market making), or

- Control of issuance order flow (launchpad / ICO platform)

has no durable moat. Liquidity is increasingly commoditized; anyone can spin up a concentrated-liquidity pool in minutes.

Raydium and Orca—once the clear category leaders—are the clearest examples of protocols caught in the middle. They are neither best-in-class active market makers nor vertically integrated issuance platforms. Their market share has steadily eroded since mid-2025, and the structural headwinds are intensifying.

Valuation Framework: Growth Path + Token Value Accrual

Raw P/S multiples are now misleading without context. The relevant questions for Solana DEX protocols are:

- Does the protocol have a credible path to sustained transaction volume growth?

- Does the token have believable value accrual to holders?

Current observations:

- WET (HumidiFi) appears cheapest on a forward basis (~2× P/S on-chain estimate), but token accrual uncertainty creates a discount.

- META (MetaDAO) trades at the highest multiple (~36× P/S) because it is one of the few tokens with credible governance and cash-flow rights.

- RAY and ORCA look expensive relative to growth prospects (10–14× P/S) given their structural disadvantages.

- PUMP and MET trade at 4–6× P/S—reasonable given issuance control, but still discounted due to uncertainty around token/equity value split and unlock pressure.

The market increasingly rewards protocols that offer both business momentum and believable token holder alignment. Tokens without clear accrual mechanics or with heavy future unlocks trade at structural discounts.

Final 2026 View: The Solana DEX Bifurcation Is Permanent

Solana spot trading will remain sharply bifurcated:

Winners:

- Active market makers (HumidiFi, Tessera) that own execution infrastructure.

- Issuance-first platforms that own the moment of token birth (Pump, MetaDAO, Jupiter DTF).

Losers:

- Standalone passive AMMs without issuance control or superior execution (Raydium, Orca classic pools).

The most durable “AMM” businesses of 2026 will not be thought of as AMMs at all—they will be issuance platforms that happen to run an AMM as their monetization layer, or execution specialists that win aggregator routing decisions.

Investors should focus capital on protocols that sit decisively at one of the two poles of the new structure. Everything in the middle faces structural decline.

Closing Thought

The Solana DEX landscape of 2026 is no longer about who builds the best AMM—it is about who owns either the moment of creation (issuance) or the moment of execution (active market making). The middle ground is disappearing. Those who recognize this bifurcation early will capture the majority of value creation in Solana’s spot trading ecosystem over the coming years. Monitor aggregator routing share, issuance volume concentration, and token accrual mechanics closely—those metrics will separate the winners from the losers in the Solana DEX race. Always conduct thorough due diligence and use regulated platforms when evaluating DeFi protocols and tokens.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.