Author: chelson Source: X, @chelsonw_

Let’s start with the conclusion: The next three years will be a major bull market led by institutions, marking the official entry of crypto and blockchain technology into Wall Street balance sheets, and mass adoption will finally be realized through a top-down revolution.

Crypto’s mass adoption will not be the anti-central bank revolution that Satoshi originally envisioned, but rather a top-down global financial infrastructure upgrade.

Retail is a tide, institutions are the ocean.

Tides can recede, but the ocean remains.

Looking Back at 2025: Why is this Bull Market the “Institutional Genesis Year”?

Reason up front: Almost all BTC/ETH capital comes from institutions; retail investors are speculating on memes and altcoins instead.

In 2025, all major coins hit new all-time highs: btc 126k, eth 4953, bnb 1375, sol 295.

1. ETF and Institutional Channels ( such as DAT) Explode

2024-2025 Large ETF Inflows

2024–2025 net inflows into digital asset funds totaled $44.2 billion, with spot BTC ETFs holding 1.1–1.47 million BTC (accounting for 5.7%–7.4% of total circulating supply).

For the first time in history, the entry point to Bitcoin has been monopolized by ETFs; retail did not participate in the main bull run.

2. Where Did the Retail Investors Go?

Structural data from TheBlock:

- In 2025, institutions accounted for 67% of BTC/ETH allocations

- Retail only 37%, primarily shifting to memecoins and low-value, short-cycle assets

Retail didn’t buy BTC/ETH; it was institutions that drove the BTC bull market.

3. How Did the Bull Market Form?

Let’s look at some data:

- Exchange BTC balances fell to a 6-year low: 2.45–2.83 million

- ETF and custody movements reduced “tradable supply” by 6.6%

- Large funds ( >$1 million ) hit a record high share of on-chain volume

This is a typical “liquidity shock bull market”: limited tradable supply + continuous institutional buying = extremely strong trend.

Why Will Institutions Go All-In Starting in 2025?

Conclusion first: Regulation is in place and institutional demand is high.

US Regulatory Clarity, First “Legal Institutional Entry” Opened

- Stablecoin Act and Stablecoin Regulatory Framework: Banks can compliantly use stablecoins like USDC/TUSD for settlement

- ETF Approval: Fully opens the floodgates for pension funds and insurance companies

These regulatory changes allow institutions to enter crypto assets legally, compliantly, and at scale.

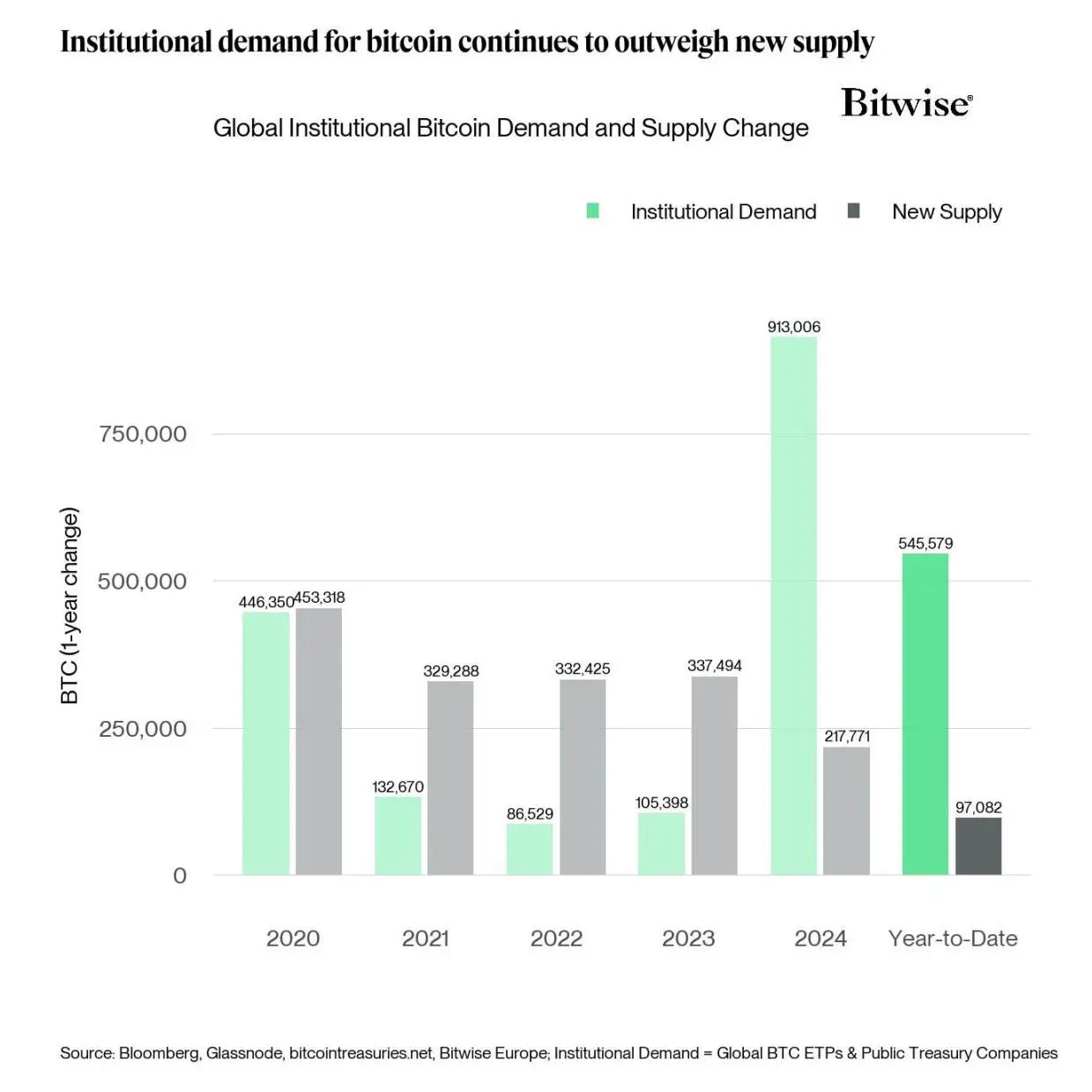

Institutional Demand Far Exceeds Supply: Structural Imbalance Amplifies

2020-2025 Institutional BTC Demand vs. Supply; Reversal Begins in 2024

Core data from Bitwise:

By 2025, effective institutional demand for BTC is about $97.6B, while actual tradable supply is only $12B, a supply-demand ratio of 80:1.

This means even without retail participation, prices can be easily pushed up several times.

In the Next Bull Market, How Will Institutional Funds Keep Flowing In?

If 2025’s cycle proves the “institution-led bull market” model, then the next three years will see this trend fully unleashed. To understand this, you have to start from the structure of traditional financial assets themselves.

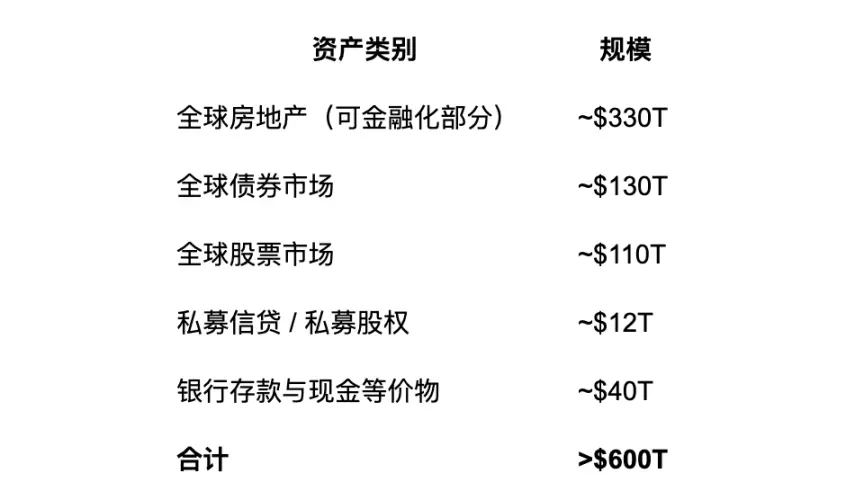

Let’s look at the total assets in traditional finance and the proportion managed by institutions to estimate the potential inflow size.

Asset Distribution in Traditional Finance Determines Who Has the “Real Money”

Global investable asset scale (2024 data):

Of which, 70%–80% is controlled by institutions (pension funds, sovereign wealth funds, insurance, banks, hedge funds, asset managers).

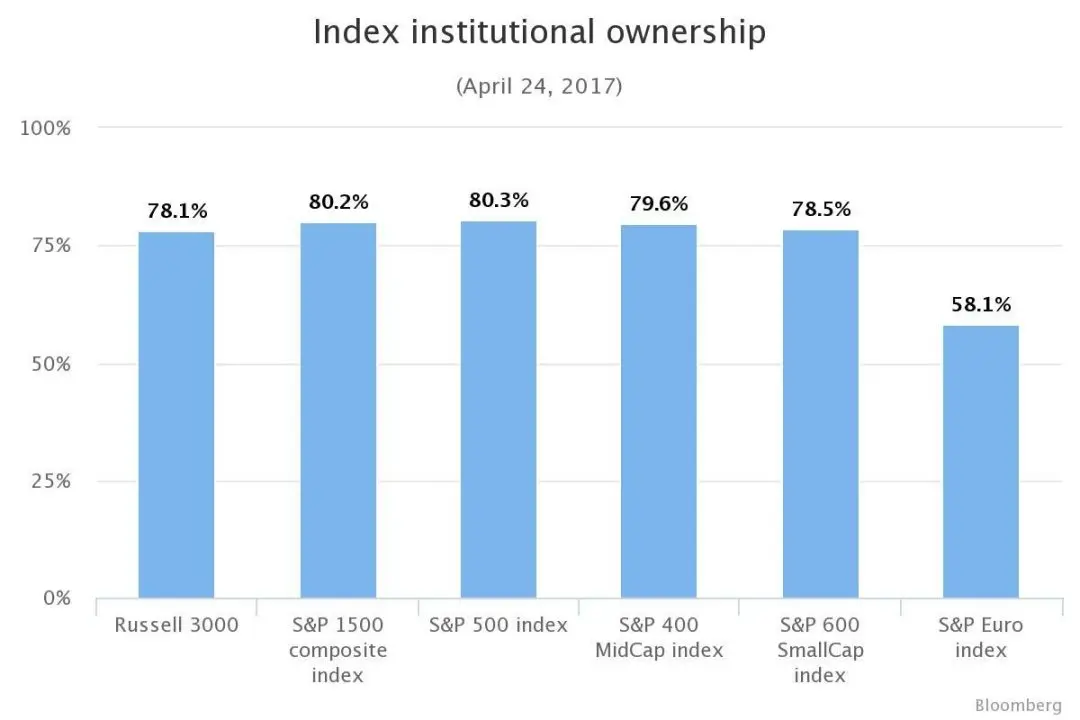

Proportion of equity assets held by institutions (2017 data)

When crypto’s underlying infrastructure connects with more than $400T( trillion ) (for comparison, BTC’s current market cap is $1.8T) in traditional assets, inflow scale is no longer about tens of billions from retail sentiment.

Every 1% asset allocation shift = trillions of dollars of capital migration = BTC market cap doubles.

That’s why ETF/RWA = the core narrative of the next bull market.

Long-Term Impact on Major Assets

Simply put, BTC becomes digital gold, ETH becomes equity.

BTC: Institutional Reserve Asset

- ETF holdings continue to rise, liquidity keeps shrinking

- Price becomes increasingly institutionalized, trend-driven, slow bull

- BTC becomes true “digital gold,” with central banks starting to hold reserves

ETH: The “Equity Asset” of the Global On-Chain Economy

Unlike BTC’s “commodity-like asset,” ETH has attributes closer to “equity”:

- ETH is a mix of inflation/deflation, trending deflationary

- ETH staking rewards are “dividends” from the on-chain economy

- ETH’s value is positively correlated with total on-chain GDP

- ETH’s valuation logic comes from “network scale × usage”

ETH’s long-term value = global on-chain economy’s market cap × ETH’s fee/tax model.

This is even stronger than tech giant stocks because it is “financial infrastructure level equity.”

How Will the Role of Retail Investors Completely Change?

Simply put, from narrative makers to price followers (for major assets; meme speculation is a separate story). Retail no longer drives bull markets, just catches the ride.

( Institutional-Led Market Characteristics:

- Trends are more stable (long-term capital)

- Emotional influence is reduced

- Liquidity is thinner (whales dominate order books)

So Retail Must Adjust Strategies:

- From emotional trading → follow big money trades

- From hunting for 100x coins → find structural, long-term opportunities

- From short-term trading → cross-cycle positioning

Where Are the Opportunities for VCs and Entrepreneurs?

The most certain tracks for VCs over the next three years:

1. Enterprise-Grade Blockchains

Simply put, no one wants pensions and bank deposits on Ethereum or Solana, so solutions for enterprise needs are required.

Enterprise requirements include:

- Privacy (public chains can’t do this)

- Compliance (KYC, AML, etc.)

- Controllability (upgradeable, revocable governance)

- Low cost & stability

Therefore, institutions can’t use public chains for core business, but must use enterprise-grade blockchain solutions (which may sound like consortium chains), e.g., Hyperledger Fabric and R3 Corda.

Institutions won’t run core business on Ethereum, but will buy BTC/ETH via ETF, DAT, RWA. Assets on public chains, business on enterprise chains, bridged by DeFi—this is the future architecture.

2. Bridging + ZK (private ↔️ public)

- Cross-chain

- Cross-market

- Cross-regulatory jurisdiction/country

- Cross-asset (RWA ↔️ public chain assets)

Enterprise blockchains need to communicate with public chains, so bridging becomes the bridge from institutional private chains to public chains. ZK technology may be the solution here, but I’m not an expert in this area so won’t comment further.

3. MPC, Custody, Asset Management Tools

Fireblocks, Copper, BitGo and similar firms will see exponential growth.

4. RWA & Settlement Layers

- Government bonds

- Private credit

- Commodities

- Foreign exchange

- Settlement layer (an on-chain version of the SWIFT network; this involves payments and is complex enough to warrant a separate article)

VCs take note, this is a trillion-dollar opportunity.

Conclusion

The next bull market is not a victory for crypto, but a victory for Wall Street.

In the next three years, you will see:

- JPM, BlackRock ###, Citi (’s on-chain scale surpass most L1s

- Retail’s influence on major coin pricing drops to historic lows

- Trillions of dollars on-chain via ETF, RWA, and enterprise chains

- Web3 shifts from narrative economy → global financial infrastructure

Crypto’s mass adoption has already happened, but not as a central bank replacement—instead, it’s an upgrade revolution for financial infrastructure.

Final Note:

Retail is dead, long live the institution.

Instead of fantasizing about 100x coins, understand the logic of capital. The next bull market will be priced by institutions, driven by enterprises, and determined by infrastructure. Retail still has opportunities, but the methods have changed. Understand structural trends and position yourself ahead of where institutions are headed.