Data from Epiq AACER, published by the American Bankruptcy Institute (ABI), shows that in the first quarter of 2026 (January to March), the total number of bankruptcy filings in the United States reached 150k, up 14% from 132k in the same period last year. Both consumer and commercial categories increased. Among them, Chapter 5 bankruptcy filings for small businesses surged 67%, the highest percentage increase across all categories.

Full Breakdown of Bankruptcy Filings in Q1 2026: A Look at Increases by Category

(Source: Equifax)

(Source: Equifax)

The growth in bankruptcy filings spans both individuals and businesses. From filing counts to category distribution, the expansion is全面:

Main Category Bankruptcy Filing Volumes and Growth Rates

Chapter 5 (Chapter 5) Small Business Reorganization: jumped from 499 to 833, a 67% increase—hit the hardest

Chapter 11 (Chapter 11) Business Reorganization: increased from 1,764 to 2,422, a 37% increase

Chapter 7 (Chapter 7) Personal Liquidation: rose to 89,259, a 17% increase

Chapter 13 (Chapter 13) Personal Repayment Plans: rose to 51,962, an 8% increase

Total Consumer Bankruptcy Filings: 141,573

Small businesses were impacted far more severely than large enterprises in this wave of bankruptcies. The 67% increase in Chapter 5 reveals that the cash-flow crunch among small and medium-sized businesses has broadly reached a tipping point.

Four Major Structural Root Causes Behind the Bankruptcy Wave

Amy Quackenbos’s analysis points to four interlocking systemic pressures—not a single event.

Ongoing Inflation: both living costs and production costs remain stubbornly high. Disposable household income is squeezed, business profit margins keep narrowing, and borrowing demand is forced upward to fill the gap.

A High-Interest-Rate Environment: the Federal Reserve’s tightening policies directly raise financing costs. Not only does the pressure for new loans intensify, but the difficulty of refinancing old debt also rises significantly, leaving many businesses and households with repayment structures that are no longer sustainable.

Credit Tightening: against a backdrop of rising bad-loan risk, financial institutions tighten lending standards. Credit channels for small and medium-sized businesses and subprime borrowers are hit first.

Global Instability: geopolitical tensions continue to disrupt supply chains and raise energy costs, suppressing consumer confidence and dampening business investment appetite.

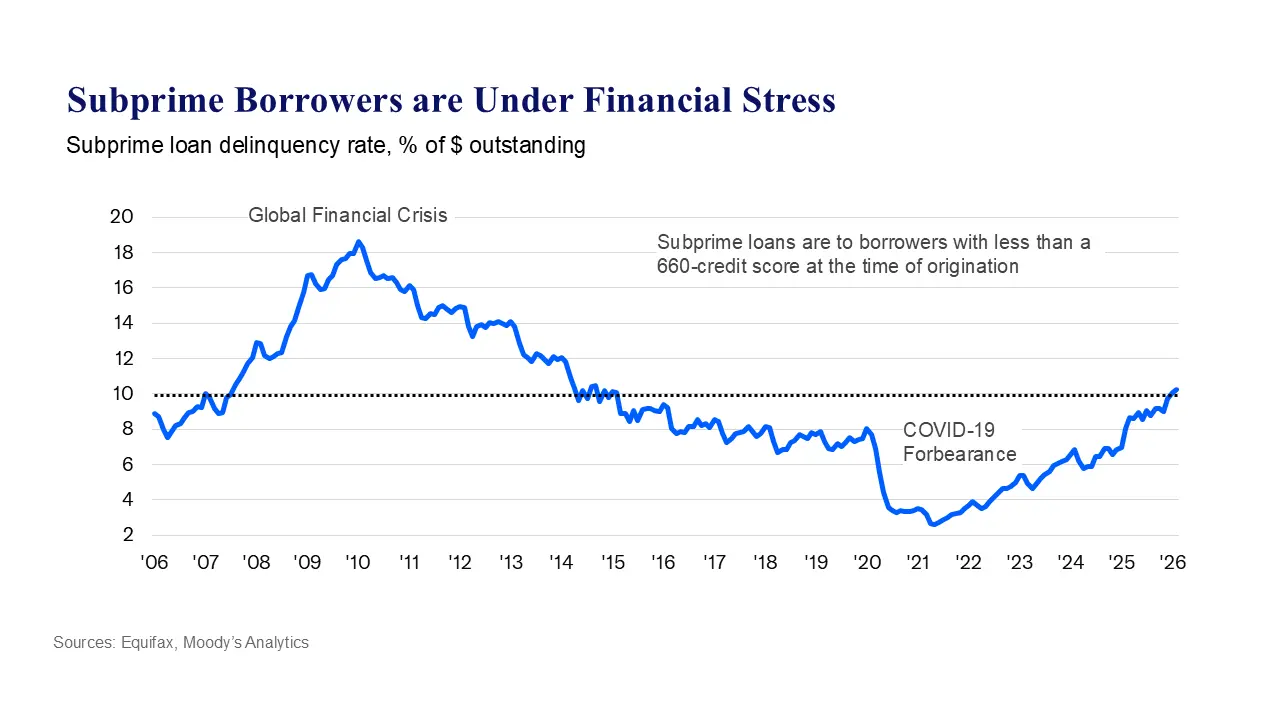

Household Financial Report data from the Federal Reserve Bank of New York provides quantitative confirmation. As of the end of Q4 2025, total U.S. household debt reached $18.8 trillion, credit card balances were as high as $1.28 trillion, and delinquency rates on mortgages and student loans also worsened significantly. As of February, more than 10% of the outstanding debt held by subprime borrowers was already in distress—this was already the case before the Middle East conflict began escalating at the current pace.

Legislative Response and Outlook: Full Relief May Be Hard Before 2027

With bankruptcy filings rising rapidly, the U.S. Congress is reviewing related response legislation. A bill jointly introduced by Senator Grassley and Representative Klein would permanently raise the Chapter 11 bankruptcy reorganization threshold to $7.5 million, and raise the Chapter 13 personal debt limit to $2.75 million, so more businesses and individuals can reorganize debts through a legal framework.

However, relief from fundamental pressures may not arrive quickly. The International Monetary Fund (IMF) projects that U.S. inflation will not fall back to the Federal Reserve’s 2% target until early 2027, implying that high borrowing costs could persist into next year. In the same period, the size of U.S. public debt has exceeded $39 trillion, further narrowing fiscal room. Whether legislative action can produce meaningful, targeted relief before the end of the second quarter remains a highly uncertain variable.

Frequently Asked Questions

What are the main reasons behind the surge in U.S. bankruptcy filings in Q1 2026?

The American Bankers Association states that this wave of bankruptcies is driven jointly by four major structural factors: continued inflation squeezes cash flow, higher interest rates raise financing costs, credit tightening restricts funds allocation, and worsening global instability increases overall economic pressure. The four reinforce each other and were not triggered by a single event.

Why did bankruptcy filings by small businesses increase as much as 67%?

Small businesses lack the financial buffer available to large enterprises. Under the dual pressures of credit tightening and high borrowing costs, cash-flow risk is more concentrated. Chapter 5 bankruptcy protection is designed specifically for small businesses, and the surge in filing numbers directly reflects the widespread deterioration of small and medium-sized enterprises’ funding chains.

When might a turning point occur in the U.S. bankruptcy wave?

The IMF projects that U.S. inflation will not fall back to the 2% target until early 2027, so the high-interest-rate environment may persist into next year. At the legislative level, a bill to raise the threshold for bankruptcy protection is still under review. In the near term, the number of bankruptcy filings may remain high, and the data trend in the second quarter will be an important indicator to watch.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.