Meta Platforms announced that it will remove Horizon Worlds from Quest headsets starting June 15. Since late 2020, Reality Labs has accumulated nearly $80 billion in operating losses, and the company plans to allocate most of its $115 billion to $135 billion capital expenditure in 2026 toward AI infrastructure.

From Rebranding to Strategic Retreat: The Final Chapter of a Five-Year Metaverse Experiment

In 2021, Facebook rebranded as Meta, signaling Zuckerberg’s strategic bet that the metaverse would be the next-generation internet. Horizon Worlds, as the flagship VR social platform, was designed as the core gateway to the metaverse—users could create virtual spaces, interact, and explore user-generated content.

However, five years later, reality is far harsher than the vision. Meta’s Reality Labs Vice President Samantha Ryan described the split as “a way to give both platforms room to grow,” but this diplomatic language masks a deeper strategic shift: the use cases for Quest headsets have shifted from social interactions to gaming and mixed reality applications, and Horizon Worlds has consistently failed to reach the expected user scale and retention on the VR platform.

Meta CTO Andrew Bosworth explicitly stated that the company will prioritize mobile experiences and wearable hardware—especially the Ray-Ban Meta smart glasses, which have demonstrated real market demand—over continued investment in immersive VR.

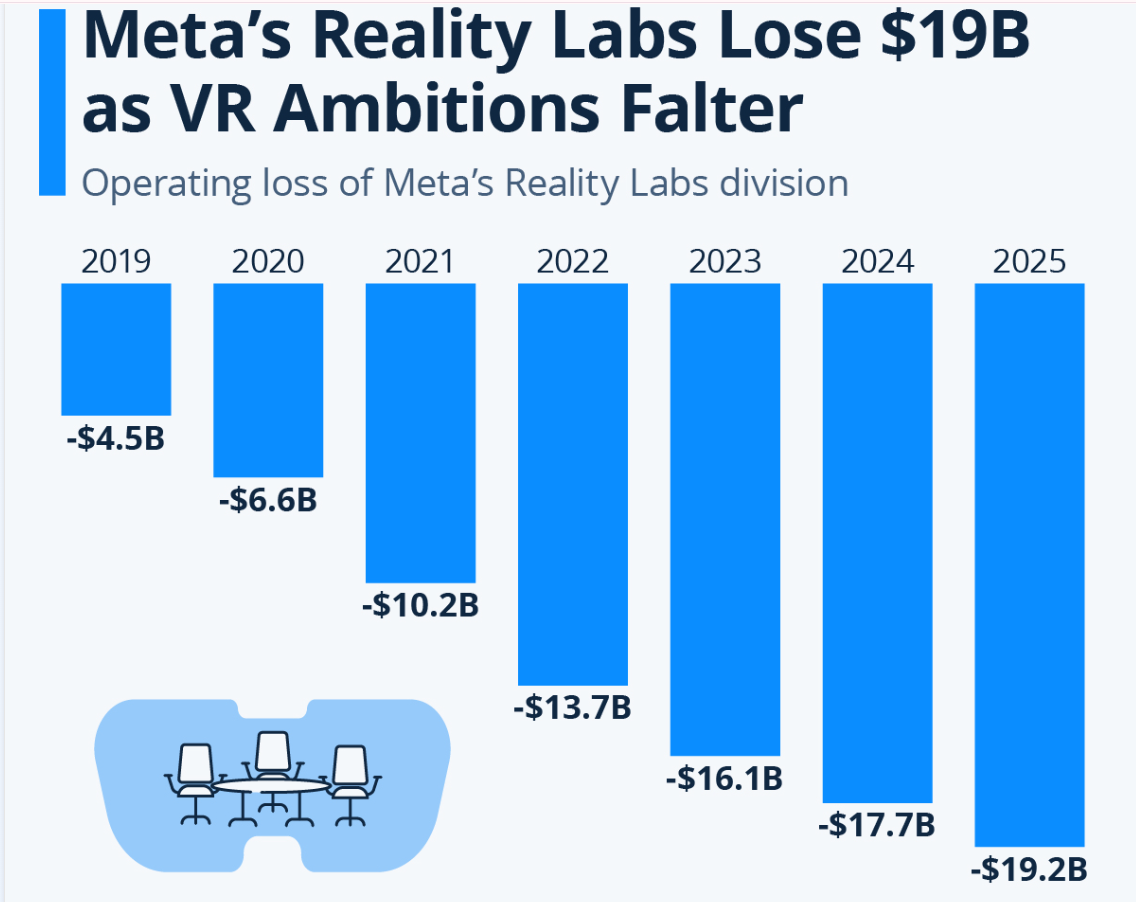

The Financial Truth Behind Reality Labs’ Nearly $80 Billion Loss

(Source: Statista)

Below are the core financial figures for Reality Labs, revealing the pressure behind the strategic shift:

2025 Operating Loss: $19.2 billion

Cumulative Loss Since End of 2020: Nearly $80 billion

2025 Full-Year Revenue: $2.2 billion (less than 12% of the loss for the same period)

January 2026 Layoffs: About 1,000 Reality Labs positions, and closure of several VR game studios

Internal Staff Turnover Goal: 20% annually from 2026 to 2027

In contrast, Meta’s advertising business remains strong—Q4 2025 revenue reached $59.9 billion, up 24% year-over-year—showing that the company’s core business engine still has the financial foundation to support its transformation. The question is whether these resources should continue to be poured into the long-term, unprofitable VR business.

Capital Flows: AI Becomes the Top Priority

Meta’s capital expenditure plan for 2026, totaling $115 billion to $135 billion, is mainly directed toward AI infrastructure and superintelligence labs. This shift from VR to AI resources is no coincidence—it reflects management’s reassessment of market opportunities: AI’s commercialization pathways (ad optimization, recommendation systems, enterprise AI tools) are far clearer than consumer adoption of the metaverse.

Every job cut in VR, every VR game studio closed, is backed by capital flowing into data centers and AI model training. Wall Street’s consensus target price for META stock is $838, reflecting market approval of this strategic pivot—yet whether this deal will ultimately pay off depends on Meta’s ability to turn large-scale AI infrastructure investments into tangible product returns before investor patience runs out.

Frequently Asked Questions

Is Horizon Worlds completely gone, or just removed from Quest?

Horizon Worlds is not entirely shut down; it has transitioned to a mobile-only platform. After June 15, users will no longer be able to create, publish, or access Horizon Worlds via Quest headsets, but the Meta Horizon mobile app will continue to provide services. This shift reduces development and maintenance costs and aligns with a larger potential user base on mobile.

Does Meta’s abandonment of VR metaverse mean the overall concept has failed?

This adjustment is a strategic shift for Meta and does not mean the entire metaverse concept has failed. Meta continues to develop Quest headsets (focused on gaming and mixed reality) and Ray-Ban Meta smart glasses, indicating the company still sees extended reality (XR) as a long-term direction—just moving from “immersive VR social” to “lightweight wearables.”

What lessons does Horizon Worlds’ failure offer for crypto and NFT metaverse projects?

Meta’s retreat from the metaverse provides an important industry lesson: user adoption barriers for VR social platforms are higher than expected, including hardware costs, comfort, and content ecosystem development cycles, which have exceeded early optimistic forecasts. For NFT and crypto projects relying on the metaverse concept, Meta’s case shows that the gap between technological feasibility and genuine user demand is even more challenging than the blueprints suggest.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.