What Stablecoins Really Mean for the U.S., Emerging Markets, and the Future of Money

Over the weekend, I couldn’t stop thinking about a recent post from @ sandeepnailwal.

It made me go back to my notes, dig into some data, and the more I looked at the numbers, the more it all started to make sense (a lot more than most people might realize).

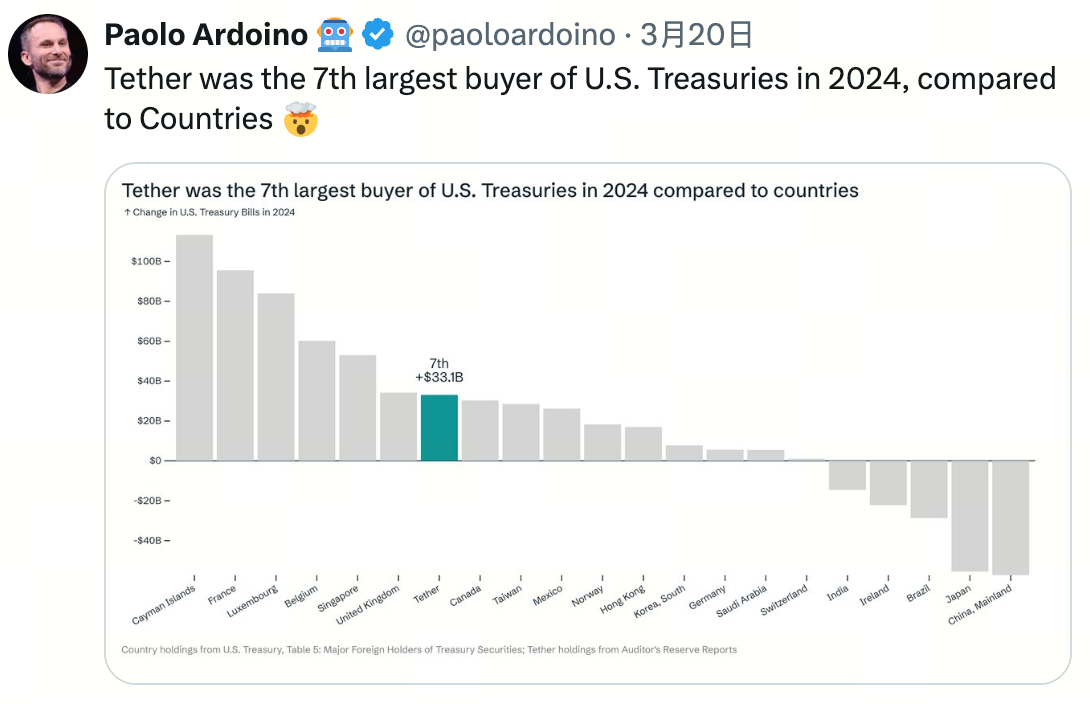

By late 2024, @ Tether_to had already become the seventh-largest foreign buyer of U.S. Treasuries, surpassing countries like Canada and Mexico in annual purchases.

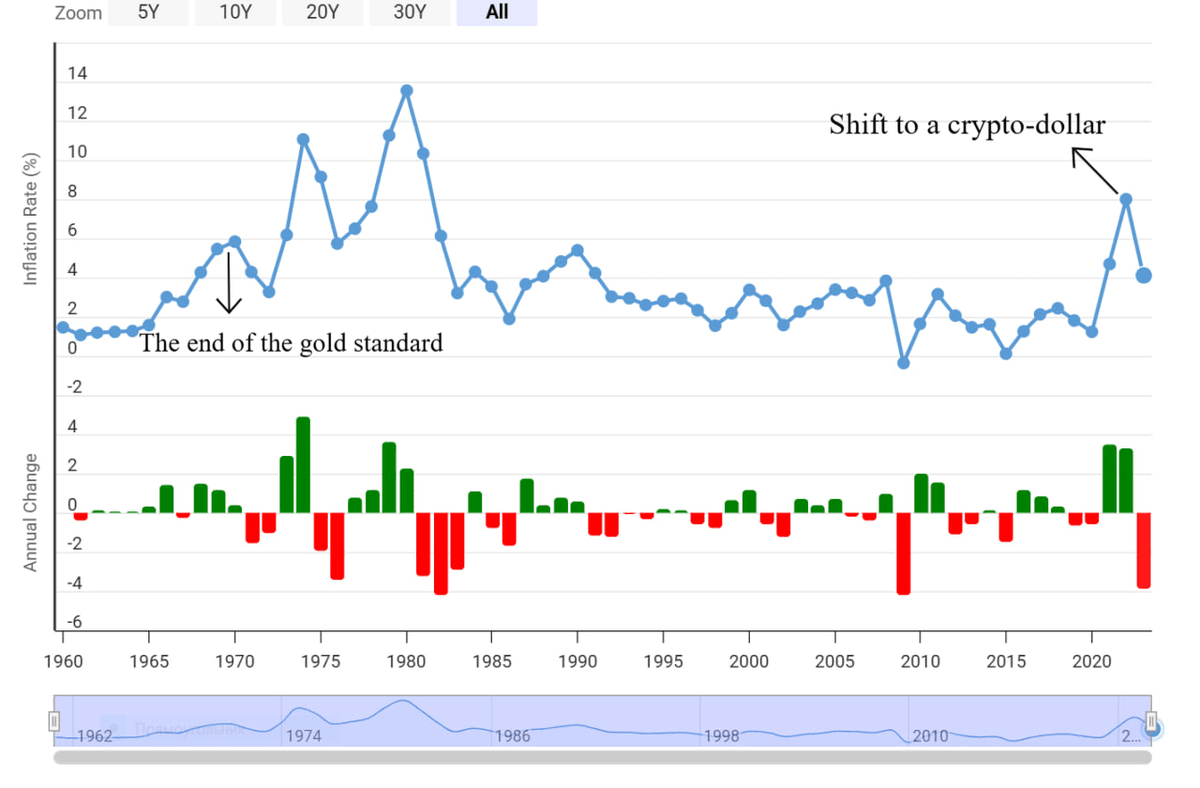

Fast forward to today, and that thesis has only become stronger. Stablecoins have quietly emerged as one of the biggest forces driving global dollar demand, while also serving as financial lifelines for emerging markets grappling with inflation, devaluation, and capital controls.

In this article, I’ll break down recent data and trends that point to the rise of “Dollarisation 2.0”

A new era beyond the petrodollar, and how this shift is shaping a world where both the U.S. and emerging economies stand to benefit, at least in the short to mid term.

We’ll see how stablecoins are rapidly becoming the “lifeblood” of global financial markets, not only within crypto but also serving as a hedge and store of value in emerging economies where local currencies are fragile.

The beginning

Stablecoins have rapidly evolved from a niche trading tool into the backbone of global crypto finance. In 2024, on-chain stablecoin transactions hit $15.6 trillion, surpassing Visa’s annual payment volume by roughly 20%. The combined supply now sits at over $300 billion, reflecting over 50% year-over-year growth. These dollar-pegged tokens, led by Tether’s USD₮ (USDT), power everything from crypto trading and DeFi protocols to remittances and everyday payments.

The appeal is simple but powerful: stablecoins combine the reliability of fiat with the speed and borderlessness of crypto, enabling near-instant, low-cost settlements across the globe.

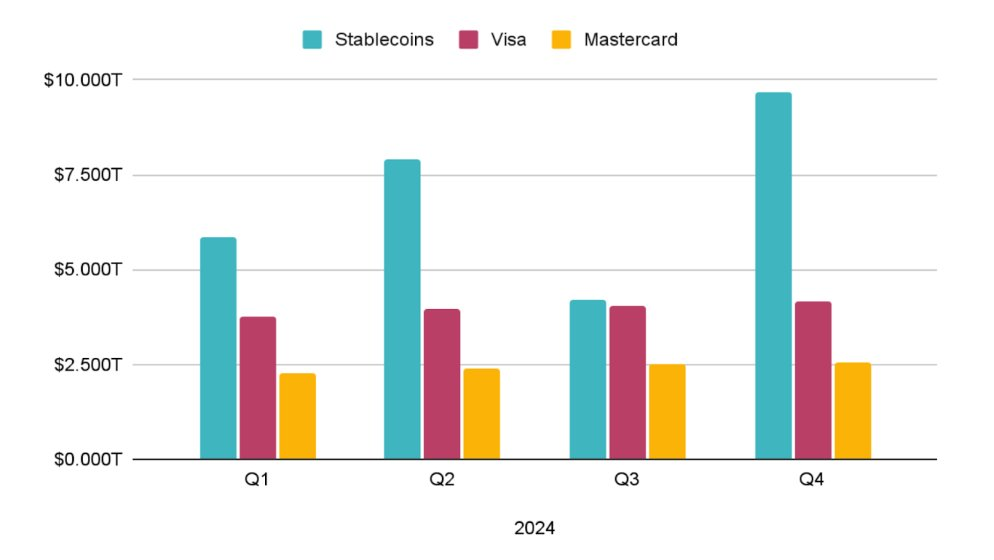

Over $100 billion in stablecoin transfers occur daily on public blockchains, and their annual volumes have rivaled or surpassed those of major payment networks. A report by CEX.io noted that stablecoin transfer volume reached $27.6 trillion in 2024, overtaking the combined volume of Visa and Mastercard by about 8%.

This remarkable usage underscores that stablecoins have achieved genuine product-market fit: users value the ability to transact in a currency pegged to the U.S. dollar (or other fiat) without the volatility of typical cryptocurrencies.

Figure: Quarterly on-chain stablecoin transfer volumes (blue) versus Visa (pink) and Mastercard (yellow) payment volumes in 2024. By Q4 2024, stablecoin networks were processing significantly more value than the major card networks. - https://blog.cex.io/ecosystem/stablecoin-landscape-3486

Several factors explain why stablecoins make sense and are growing so rapidly:

- They combine stability and familiarity by staying pegged 1:1 to fiat (mostly USD), avoiding crypto’s volatility while keeping the benefits of blockchain.

- They enable global, 24/7 transactions, settling in minutes instead of days (ideal for remittances and cross-border commerce.)

- They offer low fees, often costing fractions of a cent per transfer, making both micro and large payments viable.

- They drive financial inclusion, giving anyone with internet access a stable, accessible currency (especially in countries with inflation or weak banking systems.)

- And they’re programmable, integrating directly with DeFi for lending, trading, and earning yield.

Let’s walk through just how massive this opportunity could be.

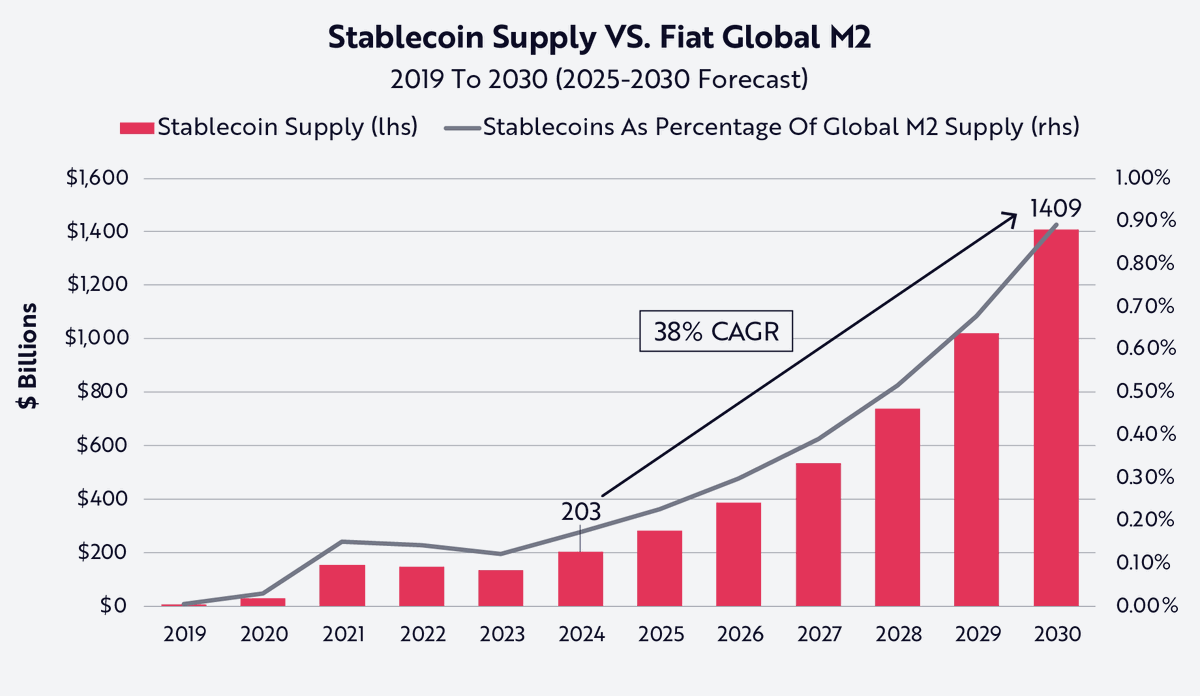

The U.S. M2 money supply is a broad measure of liquidity in the economy, including cash, checking deposits, savings accounts, small time deposits, and retail money market funds. As of mid-2025, M2 stands at roughly $22 trillion, reflecting the vast pool of dollars circulating through traditional finance.

Source: Stablecoins Could Become One Of The US Government’s Most Resilient Financial Allies

By comparison, the global stablecoin market cap is about $300 billion, or just ~1% of U.S. M2. While still small in absolute terms, this contrast underscores both the rapid growth and the enormous headroom for expansion. Stablecoins are effectively digital dollars riding on blockchain rails, and if they were to capture even a small portion of M2, the market could scale into the trillions, reshaping payments, remittances, and global dollar distribution.

Importantly, stablecoins are emerging as a complement, not a threat, to traditional payment networks.

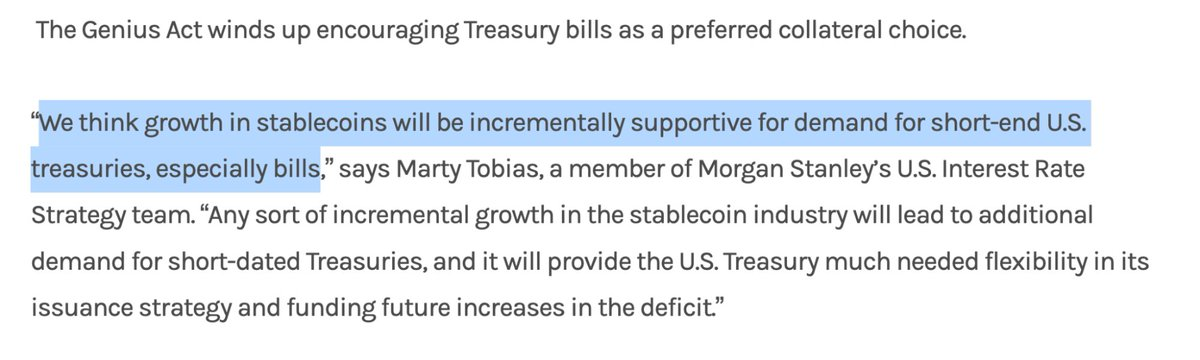

Even Morgan Stanley sees stablecoins as an incremental opportunity, noting that their growth could boost demand for short-term U.S. Treasuries, giving the Treasury greater flexibility to fund deficits and manage cash flow. These tokens can enable large-value settlements, such as interbank transfers or trade settlements, to clear almost instantly, operating like digital cash accounts.

This utility has captured regulatory attention. In the U.S., the recently enacted GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) mandates full 1:1 reserve backing with liquid assets like Treasuries or dollars, requires monthly disclosures, and prioritizes consumer protection, including safe resolution in issuer insolvency cases.

Across the Atlantic, the EU’s MiCA regulation, which took effect in mid-2024, is enforcing licensing, transparency, and reserve standards for stablecoins to bolster their stability and market integrity.

When regulated properly, stablecoins could spark a once-in-a-generation shift in how money moves, making it faster, cheaper, and more seamless, while enhancing rather than displacing legacy payment networks. (and we’re already seeing this happen)

From Petrodollar to Digital Dollar: How Stablecoins Extend U.S. Dominance

The United States has long leveraged the dollar’s reserve-currency status to reinforce its global influence, most notably through the petrodollar system, where oil exports priced in USD ensured perpetual demand for dollars and U.S. debt. Many argue that today, history appears to be repeating with USD-backed stablecoins. These crypto tokens, such as USDT and USDC, hold value 1:1 with the dollar and are largely backed by U.S. assets. By promoting dollar stablecoins, the U.S. is effectively exporting dollars at internet speed, reinforcing dollar hegemony in the digital economy in much the same way that petrodollars underpinned the oil economy decades ago.

Source: https://coinpaper.com/7398/stablecoins-the-new-petrodollar-how-trump-is-repeating-nixon-s-experience

American policymakers have explicitly embraced this trend. Under the current administration, the U.S. passed the GENIUS Act, landmark legislation establishing a regulatory framework for stablecoin issuance. The law’s intent is clear: to buttress the dollar’s status as the global reserve currency and to boost demand for U.S. Treasuries, which back stablecoins. In other words, the U.S. government views dollar stablecoins as a strategic digital dollar alliance that can cement USD dominance while financing American debt.

The GENIUS Act requires dollar stablecoins to be fully backed by safe, liquid assets such as cash and short-term Treasury bills. This means every new stablecoin issued creates a buyer for U.S. debt, a modern twist on how petrodollar surplus funds were recycled into Treasuries in the 1970s. Analysts have even described stablecoins as a “Trojan horse” for U.S. debt, guaranteeing continued and growing demand for Treasury securities from a worldwide user base.

The numbers already validate this dynamic. Tether, issuer of the largest dollar stablecoin, now holds approximately 180 billion dollars in the U.S. Treasury bills as reserves. This positions Tether among the largest holders of Treasuries globally, even surpassing the holdings of many countries.

Each USDT token in circulation represents a dollar that someone overseas is willing to hold, effectively functioning as an interest-free (almost) loan to the U.S. government when those dollars are parked in T-bills. Other issuers, such as Circle with USDC, likewise invest heavily in U.S. bonds.

This trend is so pronounced that many analysts argue stablecoins could become one of the most important strategic assets for the U.S. government over the next decade, filling the gap as foreign central banks reduce their Treasury holdings. Every time a business or individual abroad chooses to hold a USD stablecoin, they reinforce the dollar’s global role and indirectly finance America’s deficit by creating demand for short-term U.S. debt.

U.S. leaders are openly adopting stablecoins for these reasons. President Trump, upon signing the stablecoin bill in 2025, stated, “It’s good for the dollar and it’s good for the country.”

The geopolitical logic is straightforward. Just as oil-exporting nations once had to hold dollars, now anyone transacting in the digital economy might choose to use a U.S. stablecoin. In doing so, they contribute to what many describe as a next-generation petrodollar system. The U.S. benefits from both seigniorage and debt financing, as dollars flow out but ultimately return home as investment. In sum, stablecoins extend American financial influence into cyberspace: they keep the world using dollars for trade and savings, while channeling global capital into U.S. government bonds.

Importance of Stablecoins in Emerging Markets

Across emerging markets, stablecoins have become a financial lifeline, providing access, stability, and efficiency where local systems often fail. When national currencies collapse under inflation or capital controls, citizens turn to the dollar. But instead of paper bills, they increasingly reach for digital dollars that move seamlessly across borders.

Stablecoins solve three unmet needs in emerging markets

1) Dollar access without gatekeepers

Capital controls and weak banking make it difficult to hold USD in many countries. Stablecoins solve this by giving anyone with a smartphone access to a 24/7 digital dollar. In places like Nigeria and Ethiopia, businesses already use them to pay suppliers when banks and FX markets fail.

2) Cheaper, faster payments.

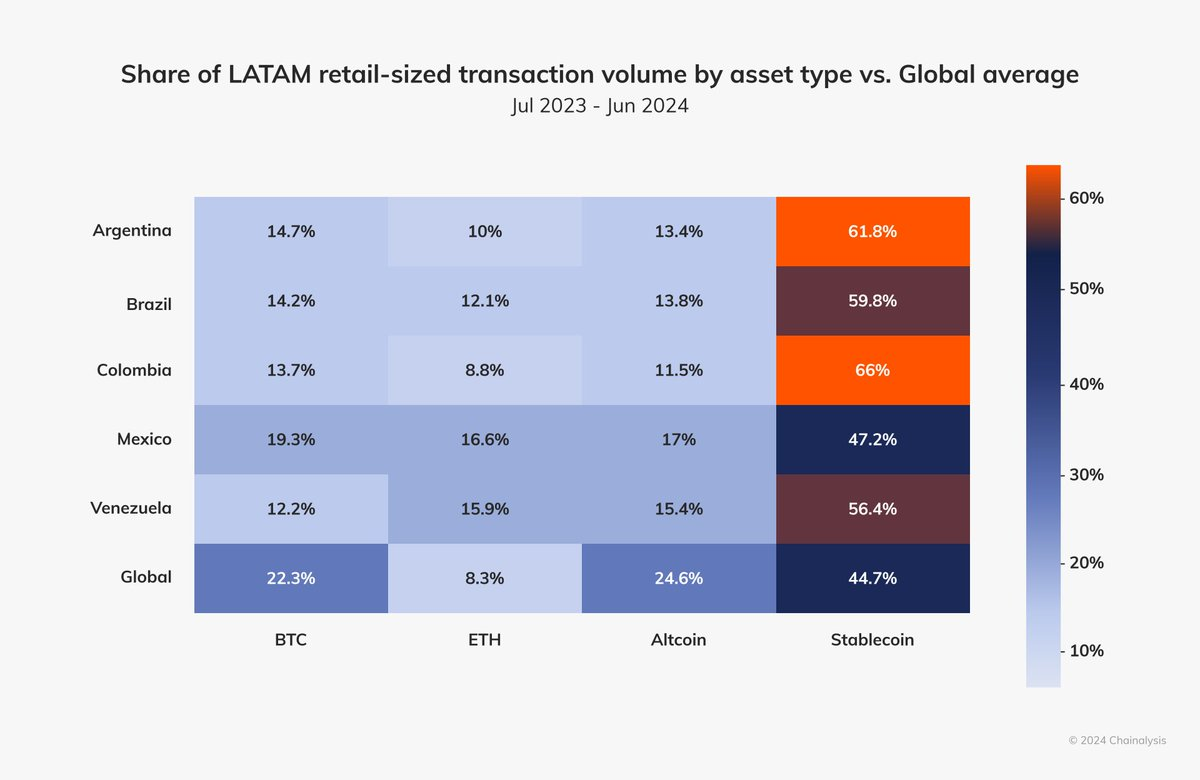

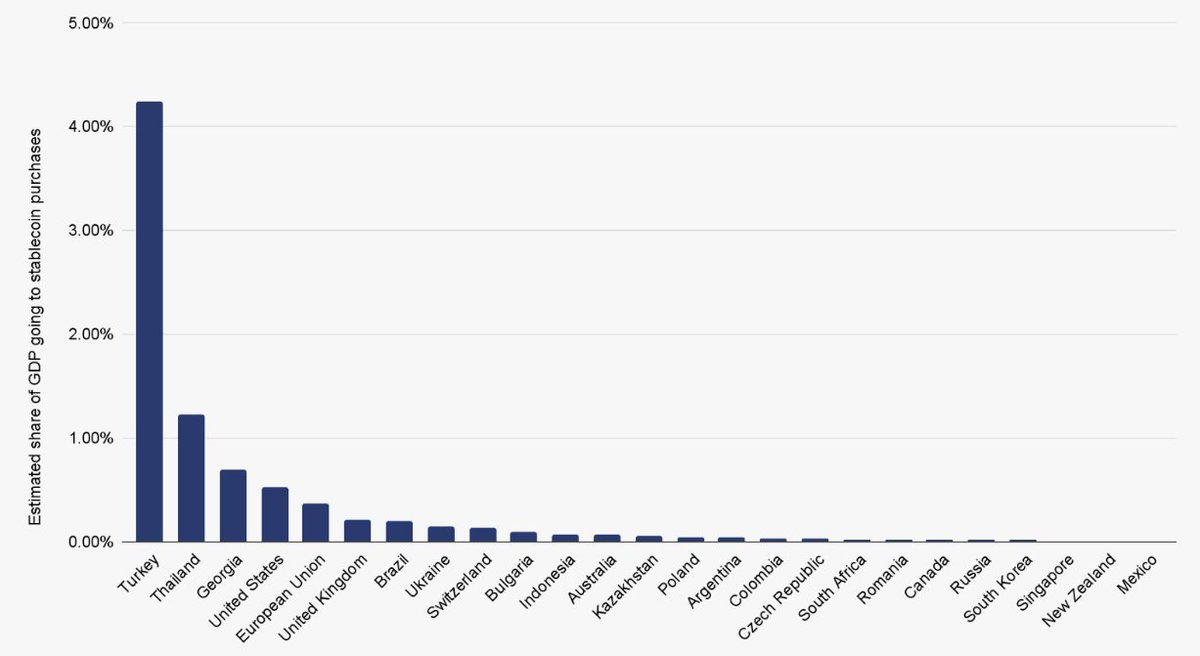

The trend is strongest where volatility runs deepest. In Argentina, more than 62% of all crypto transactions now involve stablecoins, compared to 45% last year. In Brazil, nearly 70% of exchange outflows are denominated in USDT or USDC, a reflection of how stablecoins are powering trade, savings, and payrolls. Turkey, facing inflation above 55%, saw over $38 billion in stablecoin volume last year, equivalent to 4.3% of its GDP, the highest share worldwide.

Source: https://www.chainalysis.com/blog/2024-latin-america-crypto-adoption/#:~:text=America%20region,7

Turkey, where inflation has also run above 60 %, has seen adoption on an unprecedented scale. Between April 2023 and March 2024, Turkish stablecoin purchases reached 4.3 %of the country’s GDP, the highest ratio in the world, with around 38 billion dollars in purchases over that period. Stablecoins now account for more than half of crypto transaction volume in many emerging markets, even eclipsing major assets such as Bitcoin.

Source: https://cointelegraph.com/news/stablecoin-buys-turkey-4-percent-gdp

This year, Flutterwave, Africa’s largest payments processor handling over $40 billion annually, chose Polygon as its default blockchain for cross-border stablecoin settlements across 30+ countries. The partnership is one of the largest real-world deployments of stablecoins in history, powering both consumer and enterprise flows for major clients like Uber and Audiomack.

The trend is even clearer globally. Across LATAM, Africa, and Southeast Asia, Polygon powers over 50–70% of non-USD stablecoin activity. Millions rely on Polygon’s rails for instant remittances, daily purchases, and gig-economy payouts in regions where legacy financial systems remain slow, costly, and fragmented.

3) A stable unit of account.

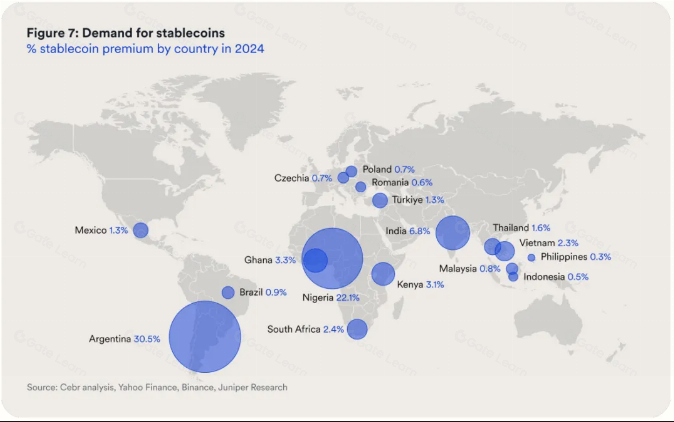

High inflation makes local pricing impossible. In Argentina, ~62% of crypto activity is in stablecoins and USDT has traded at a premium to the official USD rate.

In Asia, Polygon’s adoption is accelerating across both fintech and government layers. Japan’s JYPC introduced the world’s first yen-pegged stablecoin, deployed on Ethereum, Avalanche, and Polygon, with Polygon leading in daily transaction volume and active user addresses.

In stressed markets, demand is so strong that people even pay a premium above the U.S. dollar’s face value just to secure tokenized dollars. In Argentina, USDT has traded for up to 30% more than the official exchange rate, underscoring how much people trust digital dollars over local banks or government guarantees.

The momentum now extends beyond retail adoption. Polygon has become the institutional on-ramp for stablecoins and Real-World Assets (RWAs). BlackRock’s BUIDL Fund, the world’s largest tokenized U.S. Treasury product with $3 billion in assets, deployed $500 million on Polygon, its largest allocation outside Ethereum.

Franklin Templeton’s FOBXX Fund (worth over $300 million) also runs on Polygon, using it as the execution layer for tokenized U.S. Treasury exposure.

While Ethereum continues to hold its position as the institutional-grade network for programmable money, @ 0xPolygon is emerging as a clear leader in emerging markets and one of the top choices globally for scalable, low-cost infrastructure.

Polygon’s recent payments activity reflects this momentum. In October 2025, Polygon’s on-chain transfer volume reached an all-time high, with:

- App transaction volume up 20% month-over-month

- On/off-ramp activity up 35%

- Card payments up 30%

- Infrastructure usage up 19%

In total, the network processed 128.8 million transactions across 3.01 million active addresses, with a stablecoin market cap of $3.1 billion, placing it firmly as the third-largest stablecoin network globally, behind Ethereum and Tron.

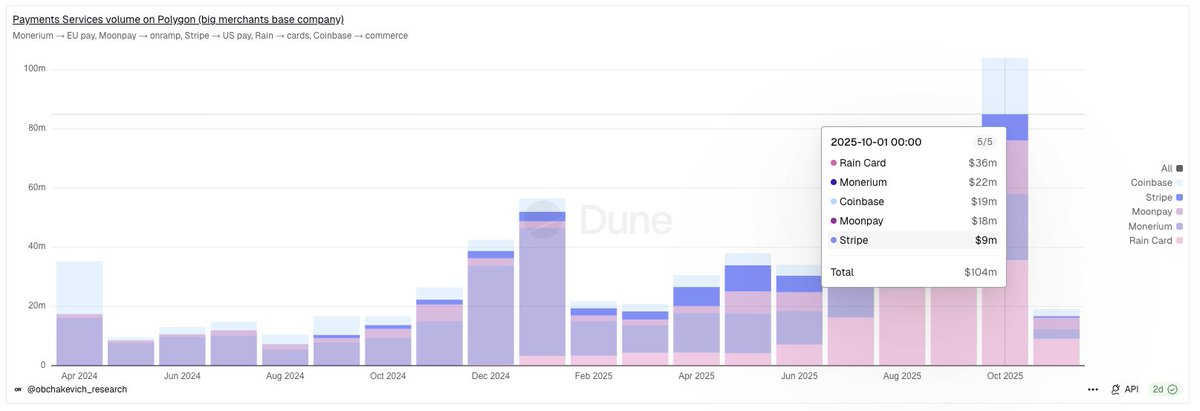

Polygon’s strength lies in its diversity. Stripe, the world’s largest fintech payment processor, now handles over $8 million in monthly volume through Polygon integrations, alongside @ Coinbase, @ Moonpay, @ RainCards, and @ Paxos, all leveraging Polygon’s rails for stablecoin and settlement flows.

Closing thoughts

The story of stablecoins is no longer theoretical. It’s unfolding in real time as billions (and soon trillions) move across networks like Ethereum and Polygon, reshaping how the world stores, transfers, and settles value. From U.S. Treasuries to gig worker payments in Lagos, the same rails now serve vastly different economies under one digital standard: the dollar.

In the medium to long term, how this transformation unfolds remains to be seen. What is clear, however, is that stablecoins have already established themselves as a core building block of the new financial internet, one that continues to bridge institutions, markets, and individuals in ways traditional systems never could.

As i always keep saying

These aren’t just arbitrary numbers, they hold real value and impact for millions of people from emerging economies who rely on these rails.

Disclaimer:

- This article is reprinted from [0xyanshu]. All copyrights belong to the original author [0xyanshu]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Share

Content

Related Articles

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

What is Stablecoin?

Top 15 Stablecoins

A Complete Overview of Stablecoin Yield Strategies

Stripe’s $1.1 Billion Acquisition of Bridge.xyz: The Strategic Reasoning Behind the Industry’s Biggest Deal.