Replaying the Neobank Mistake in Crypto Or Rebuilding It Right?

Failure of neobank 1.0 and how most crypto neobanks are walking on a similar path, but crypto (maybe) can save the neobank business.

Do you know that less than 5% of neobanks are profitable?

Neobanks have an alluring pitch: fully digital banking with lower fees and better user experience. However, the economics of these digital banks have proven fundamentally weak.

Here is a deep dive into why a lot of traditional neobanks struggle to be profitable, and crypto neobanks are following the similar path.

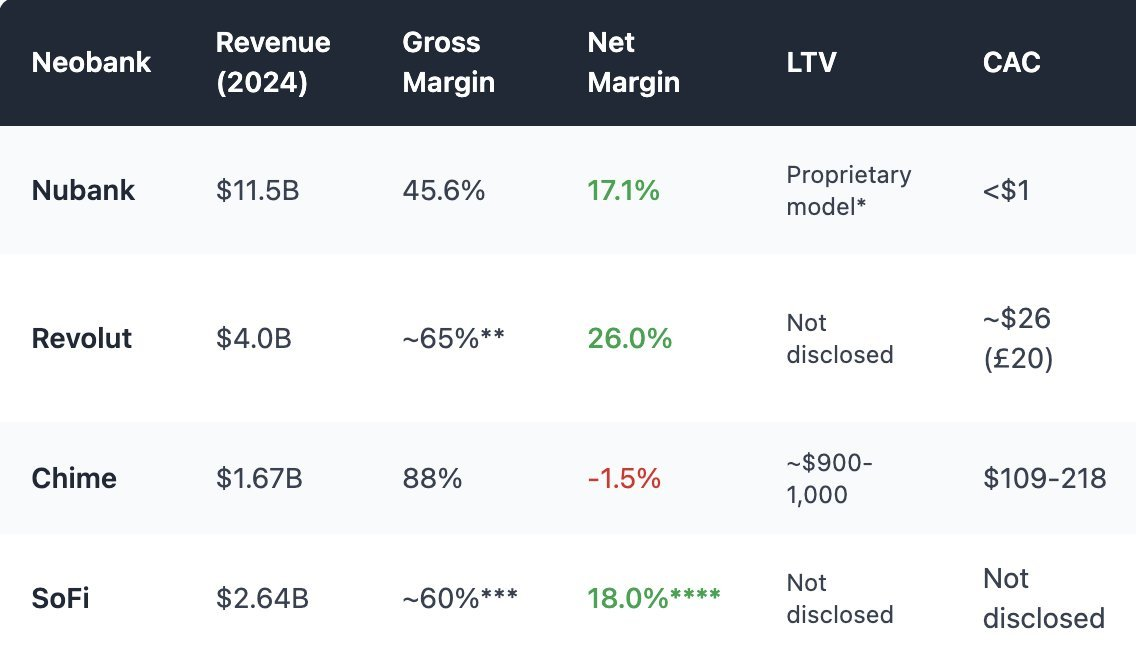

Image from @ ashwathbk (https://x.com/ashwathbk/status/1975899128745054710)

1. Overreliance on Interchange Fees

Neobanks revenue depends overwhelmingly on interchange fees, the small cut earned each time a user swipes their debit card.

This works at scale, and only if margins hold and spending volume is high. However, most of the time in practice, the economics are thin and fragile.

Chime, the U.S.-based neobank with no banking license of its own, can only rely on partner banks to hold deposits and issue cards, very similar dynamics of that in crypto neobanks. Its business model is laser-focused on card transactions. In 2024, ~80% of total revenue is from interchange fees.

However, regulators in many regions have capped interchange rates:

- EU: 0.2% per transaction

- U.S. (Durbin Amendment): ~$0.21 + 0.05% per swipe

- Chime uses small-bank partners to charge up to ~$0.44/swipe

But this legal arbitrage is under pressure, and the margin is slim to begin with for neobanks to rely on interchange fee to be a sustainable business model.

Besides, Interchange income is also highly sensitive to consumer spending cycles. In an economic downturn, if people spend less on their cards, neobank revenues dip.

2. Idle Capital: No Lending, No Interest Income

The core of banking revenue is interest income from lending, not payments.

Traditional banks transform deposits into loans, earning interest on mortgages, credit lines, and business financing.

Neobanks, even those with a banking license, have largely failed to build this core function.

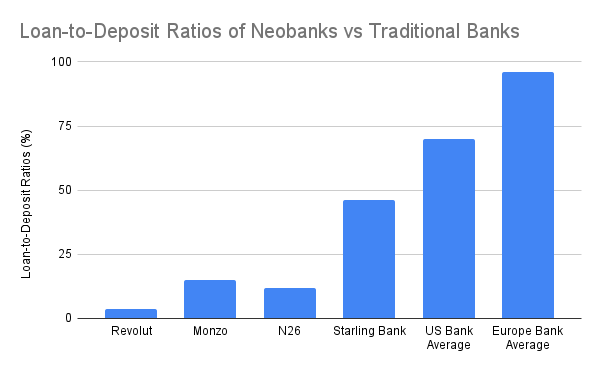

Traditional banks generate 60-65% of their revenue from net interest income, with a loan-to-deposit ratio of 55-65%, and even higher globally on average. However, most neobanks fall short in this main revenue stream, except for Starling Bank because of its acquisition of a mortgage portfolio.

Running on self-custody model, crypto neobanks would have no ability to receive interest income on deposits. They can’t touch the user’s funds to generate yield. At best, they pass deposits through to DeFi protocols like Aave or Lido, taking a small portion of the yield as a commission. However, these integrations offer no underwriting, no real control, and carry their own risk vectors, such as protocol hacks, stablecoin depeg, etc.

In both fintech and crypto models, the same paradox repeats: deposits pile up, but can’t be monetized.

Essentially, many neobanks, including crypto neobanks, are just expensive storage units for deposits.

3. High CAC and Maintenance Costs

Unlike incumbent banks that grow organically throughout history or via branch networks, neobanks must win each customer through marketing and referrals in a crowded digital marketplace. This has led to high customer acquisition costs (CAC) that severely squeeze their economics.

Cost for crypto neobanks to acquire customers would only be higher because of the onboarding barrier and education required. Not to mention, most are using high APY and token incentives to attract users to deposit into the app. That is a deferred liability for the company to pay back and significantly increase CAC.

The cost-to-revenue ratio for crypto neobanks is also worse than that of traditional neobanks:

- Stablecoin-based payments shrink FX and interchange margins, a race to the bottom amid growing competition

- Regulatory obligations, even for self-custodial models, require KYC, off-ramp controls, and card program compliance. If card spend usage is found fradulent, the chargeback and penalty would be charged to the crypto neobanks. They might even risk service halt by the centralized card issuers.

- Most users are low-balance retail (<$1,000 in deposits), while support, fraud, and infrastructure costs remain fixed.

4. Rebuilding the Model: Winning with Embedded DeFi

Crypto neobanks won’t win by emulating Chime or Monzo because the foundation of the business is different, given the self-custodial nature of crypto neobanks. I do not think crypto neobanks have edge over traditional neobanks, but crypto can help make neobanks more profitable through embedded DeFi.

1. Trading Activity as the Main Source of Revenue

Trading revenue has become a proven way to drive high-margin revenue for both traditional neobank and crypto wallets.

- Revolut Wealth Division (including crypto, in 2024): £506 million (16.3% Total Revenue), up 298% YoY, driven by customers speculating on crypto rather than traditional banking services.

- Phantom Wallet (projected 2025): $79 million from in-wallet swaps

Embedding trading has already been seen as a standard feature in the industry. App would need to provide a wide asset range, trading pair, MEV protection, fast execution, etc to stand out and ensure users have the best experience trading.

2. Structured Yield & Onchain Wealth Products

Rather than lending directly, neobanks can package complex DeFi products into wealth products that is easy for retail users to understand and invest in.

- Self-issued stablecoin, earning T-bill yield by prompting users to swap into neobank’s stablecoin

- Curated yield vaults and Retail Saving Protocol

- Onchain ETF/ RWA

- Insurance

I have not seen many Western neobanks able to replicate the success of the Alipay Wealth product suite.

Screenshot of Alipay wealth product offering

Crypto neobanks have an edge in offering a wide range of wealth management products that could simplify DeFi and make high yield financial products more accessible to a broader audience.

Embedded DeFi can help enrich neobank wealth product suite.

Conclusion: Don’t Build the Bank. Build the DeFi Rails.

Neobanks have always operated on thin margins. Crypto neobanks, despite DeFi-native tooling, face even steeper odds: thinner fees from stablecoin payments, higher compliance costs, tougher onboarding, and crowded competition once traditional neobanks flip the crypto switch.

As Revolut and Nubank start offering stablecoin, crypto trading and onchain yield alongside existing infrastructure, crypto-first neobank will struggle to compete for user mindshare.

The winning opportunity does not lie not in building another neobank but in supplying the rails: yield routers, stablecoin FX layers, DeFi wrappers or curators that plugs into existing banking distribution. It is difficult to compete with neobanks that have already amassed a wide user base, but we should strive to complement and enhance their profitability with crypto.

Disclaimer:

- This article is reprinted from [0xcoconutt]. All copyrights belong to the original author [0xcoconutt]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?