Gate Research: Funding Plunges 49.5%, Industry Enters a New Phase of Stabilization and Divergence | August 2025 Web3 Fundraising Overview

This report summarizes Web3 industry funding in August 2025. A total of 112 deals were completed, with total funding reaching $2.05 billion, marking a clear decline from previous periods. CeFi once again demonstrated strong capital absorption, infrastructure and mid-sized growth projects received steady support, while application-layer projects faced accelerated elimination. With the emerging trend of “on-chain reserve assetization” and institutional capital increasingly concentrated in Series B and strategic rounds, the Web3 industry is entering a more stable, diversified, and sustainable growth stage. The report also highlights major funding cases, including SuperGaming, Multipli, BOB, HoneyCoin, and Perle.Summary

- According to data released by Cryptorank on September 16, 2025, the Web3 industry recorded 112 funding deals in August 2025, with a total amount of $2.05 billion, marking a significant decline compared with previous months.

- Among the top 10 funding deals, traditional capital market instruments (IPO, convertible bonds, PIPE) emerged as the primary financing methods. Thematic focus shifted to “on-chain reserve assetization”, with several listed companies incorporating public chain tokens into their financial strategies.

- The funding landscape showed a pattern of “CeFi dominance, steady growth in foundational services, and overall pressure on the application layer.” CeFi led with $1.3 billion in funding, followed by blockchain infrastructure services with $240 million.

- Funding scale continued the trend of “smaller-ticket deals as the majority, with high concentration among large deals.” Investment remained centered on growth-stage projects, with deals in the $3–20 million range accounting for 58.8% of the total.

- In terms of funding stages, early-stage investment remained active and strategic deployments stood out. Seed and strategic rounds together made up nearly 70% of total deals, reflecting investors’ strong focus on innovation potential and ecosystem synergy. Unlike July, where Series A dominated, August saw funds flow more heavily into Series B, which, while accounting for only 9.3% of deal count, absorbed 45.7% of total funding, making it the month’s biggest “capital magnet.”

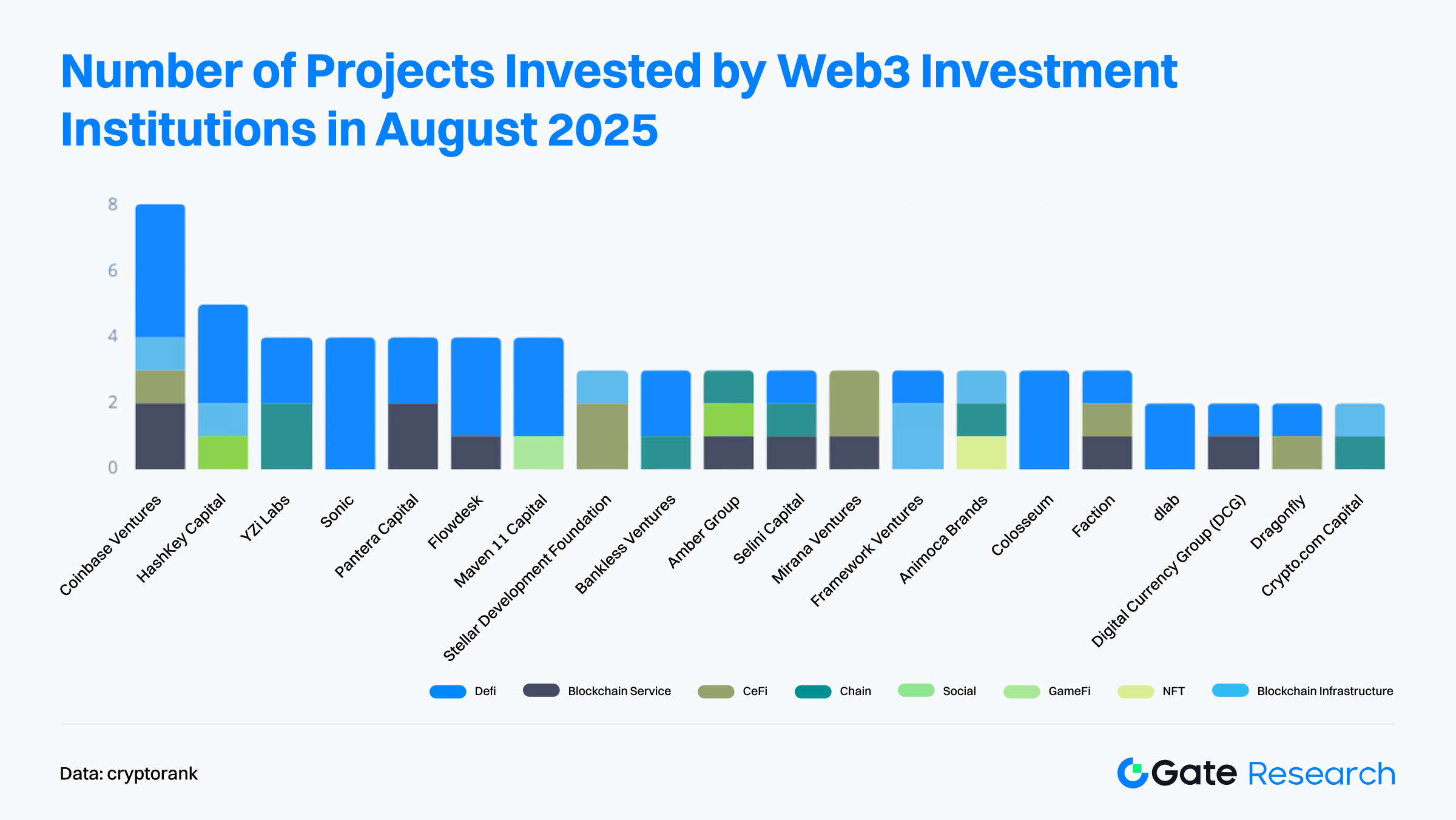

- At the institutional level, the most active investors were top-tier venture funds and industry-focused capital. Coinbase Ventures led with 8 deals, spanning DeFi, blockchain infrastructure, and CeFi, consolidating its presence across core verticals.

Financing Overview

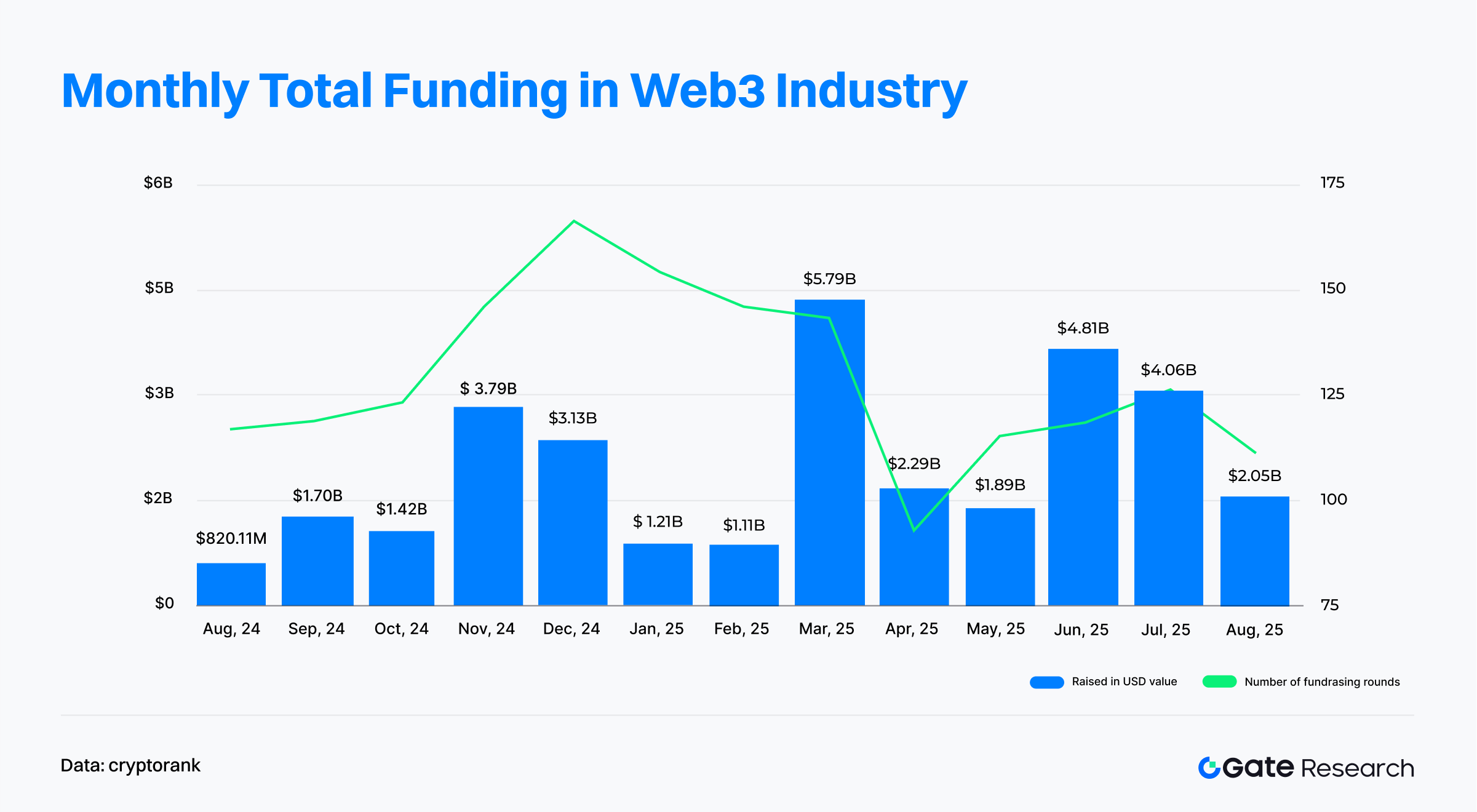

According to Cryptorank’s data published on September 16, 2025, the Web3 industry recorded 112 funding deals in August 2025, with a total amount of $2.05 billion.【1】Due to differences in Cryptorank’s statistical methodology, this figure differs slightly from the sum of individual disclosed deals (approximately $4.51 billion). To ensure consistency, this report uses the original dashboard data.

Compared with July’s 126 deals totaling $4.06 billion, the number of deals in August declined by 11.1% MoM, while the funding amount plummeted 49.5% MoM, nearly halved. Looking at the yearly trend, fundraising surged rapidly at the beginning of 2025, peaking in March at $5.79 billion, largely driven by regulated financial services, listed company expansions, and deeper integration with traditional finance. However, after the peak, capital cooled quickly, with April funding dropping sharply to $2.29 billion, alongside fewer rounds, signaling a market wait-and-see period.

Mid-year, fundraising partially recovered: June and July saw funding bounce back to $4.81 billion and $4.06 billion, respectively. Several listed companies raised capital through stock or convertible bond issuances to build crypto reserves, pushing July’s deal count to the second-highest in nearly a year and refocusing capital on mature tracks and leading projects. Yet, August again tightened, with total funding falling back to $2.05 billion. Large-scale financings significantly decreased, with only Bullish’s $1.1 billion IPO topping the list. Deals above $500 million numbered just three. Overall, while fundraising volume fell sharply, it remained higher than at the start of the year, showing that market interest persists—though capital allocation strategies have clearly shifted.

In summary, the Web3 fundraising market in H2 2025 is undergoing a structural adjustment. Capital is moving from “frenzied big bets” toward “steady, diversified positioning.” Despite the drop in total funding, the continued high level of deal activity shows that investor confidence remains intact, and the industry is entering a more rational and sustainable growth phase.

While fundraising cooled overall in August, the Top 10 largest deals still highlighted clear structural trends. The largest deal was Bullish’s $1.1 billion IPO, accounting for more than half of the month’s total funding and underscoring the strong appeal of institutional-grade CeFi platforms in capital markets. Next was TeraWulf’s $850 million convertible bond to expand Bitcoin mining infrastructure, reflecting ongoing capital bets on energy and computational power assets.【2】

Among strategically transforming listed companies, Verb Technology ($558M PIPE, with TON as reserve asset), SharpLink ($400M stock issuance, with ETH as reserve), and DeFi Development Corp. ($125M issuance, with SOL as reserve) raised over $1 billion in aggregate, highlighting the trend of “corporate treasury-ization of crypto assets”—where traditional listed companies increasingly adopt public blockchain tokens as strategic reserves.

Infrastructure and application-layer projects also saw notable deals: Satsuma Technology raised $218M via convertible bonds to develop blockchain indexing services; Rail was acquired by Ripple for $200M, signaling accelerated consolidation in the payments sector; Story Protocol secured $82M in a token acquisition to advance intellectual property tokenization. Emerging tech-Web3 crossovers also drew attention: IVIX ($60M Series B, AI + public data compliance analytics) and Rain ($58M Series B, payment card issuance) both secured growth capital in niche verticals.

Overall, August fundraising revealed two clear trends:

- Traditional capital market instruments (IPOs, convertible bonds, PIPEs) became the dominant financing channels, showing CeFi’s deepening integration with traditional finance.

- “On-chain asset reserves” emerged as a hot theme, with multiple listed companies incorporating public blockchain tokens into their financial strategies.

Although total funding dropped sharply month-over-month, leading projects still managed to secure mega-deals, suggesting that capital is concentrating on companies with compliance readiness, infrastructure attributes, and clear business models.

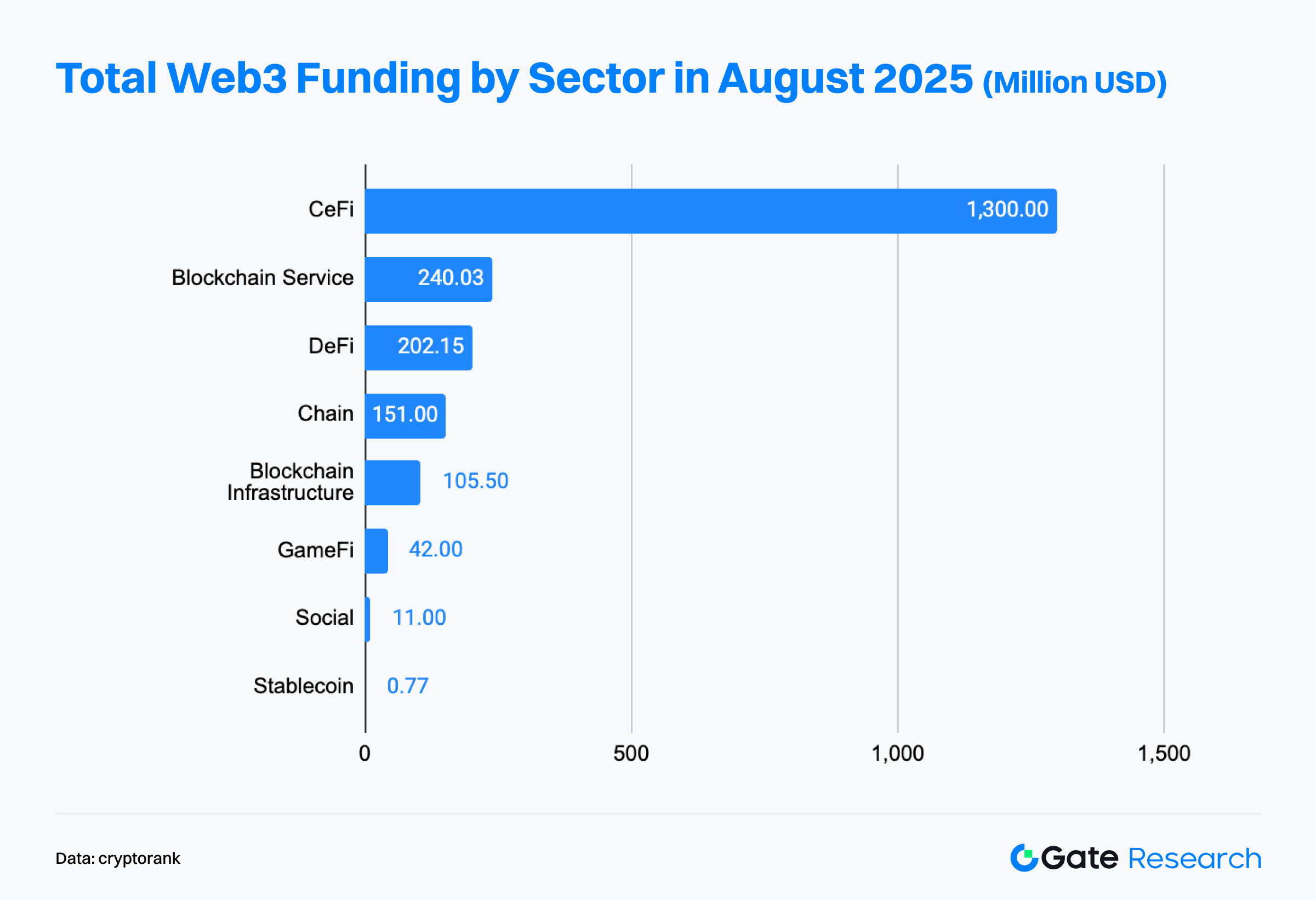

According to data from the Cryptorank Dashboard, the Web3 fundraising market in August 2025 showed a clear pattern: CeFi dominated, blockchain services continued stable expansion, while application-layer tracks came under pressure.

Centralized finance (CeFi) led by a wide margin with $1.3 billion in funding, accounting for over 60% of the total, largely driven by the Bullish IPO as well as multiple stock issuances and convertible debt financing by listed companies. This reflects the market’s view of CeFi as a key gateway for integrating traditional finance with Web3, backed by strong confidence in its compliance and scalability.

Blockchain services followed with $240 million, benefiting from their “infrastructure” attributes, covering emerging areas such as data indexing and AI-powered compliance analysis. This demonstrates that capital remains bullish on technology platforms that provide fundamental support for developers and enterprises.

The DeFi sector ranked third with $202 million, underscoring its continued long-term appeal as a core component of Web3 applications. Meanwhile, Chain ($151 million) and Blockchain Infrastructure ($106 million) maintained steady funding volumes, indicating sustained optimism about the long-term value of base-layer scaling and technological innovation.

By contrast, funding for GameFi ($42 million), Social ($11 million), and Stablecoins (less than $1 million) remained subdued, highlighting the clear retreat in enthusiasm for application-layer and experimental tracks. Investors have become more cautious, focusing on high-quality projects with sustainable business models and well-defined growth paths.

Overall, the August fundraising landscape reaffirmed CeFi’s strong capital-magnet effect while underscoring investors’ lasting preference for foundational services and key platforms. Application-layer tracks, however, have entered a phase of differentiation and adjustment, with investors accelerating the filtering process to back projects with real value and long-term potential.

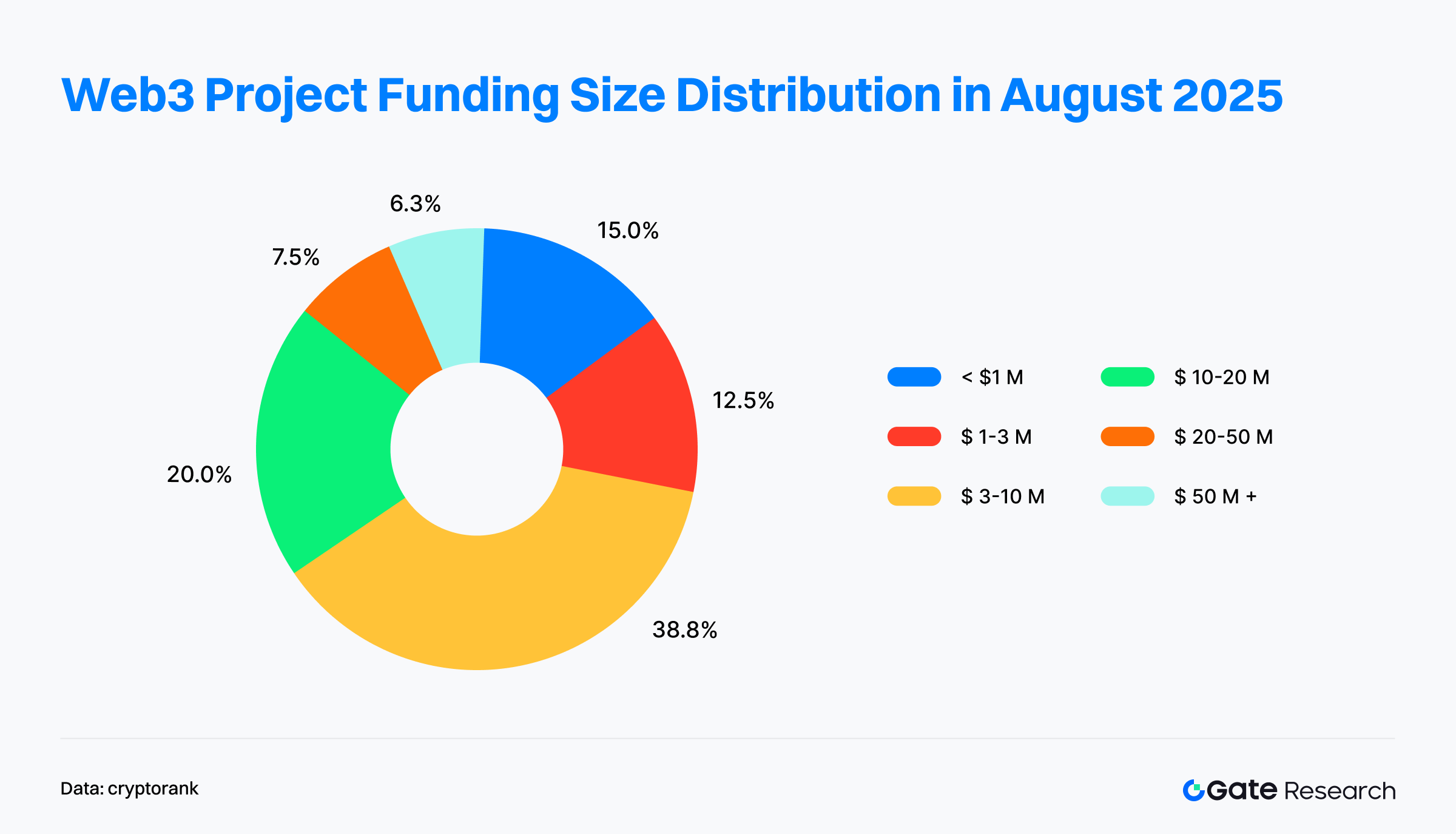

Based on financing scale data disclosed for 80 Web3 projects in August 2025, the market continued to follow a pattern of “small- to mid-sized fundraising as the majority, with large deals highly concentrated.” Investment focus remained on growth-stage projects.

Projects raising between $3 million and $10 million were the most numerous, accounting for 38.8% of the total; combined with the $10 million–$20 million range, the share reached 58.8%, underscoring investors’ strong preference for mid-sized projects that have moved beyond the early stage and show clear growth potential.

In comparison, early-stage deals below $1 million (15%) and in the $1 million–$3 million (12.5%) range were relatively limited, reflecting greater caution toward “pure concept” projects.

Although deals over $50 million made up only 6.3%, their sheer size allowed them to dominate total funding, proving that leading enterprises still maintain strong fundraising power.

In summary, August fundraising trends reflect a dual dynamic: on one hand, broad-based allocations into medium-scale projects to diversify risk and capture growth opportunities; on the other, heavy capital concentration in a handful of industry leaders. Web3 investment is shifting from “broad-based bets” to a “top-concentrated + long-tail distributed” dual-track model, highlighting investors’ increasing focus on maturity and sustainable business models, as industry competition accelerates into a survival-of-the-fittest phase.

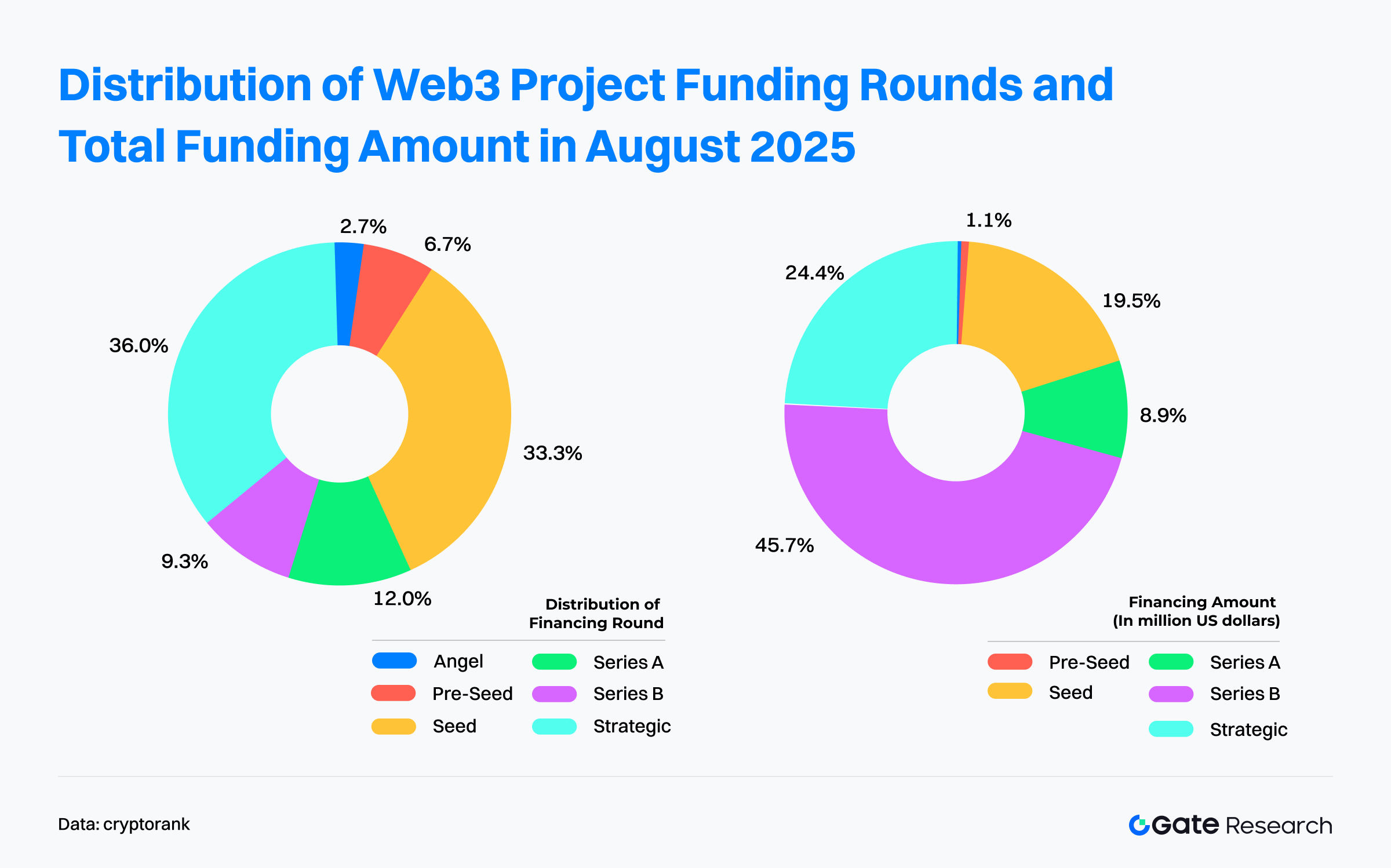

Based on financing data from 73 Web3 projects disclosed in August 2025, the market showed a clear structural pattern of “early-stage projects dominating in number, while later-stage projects dominate in capital raised.”

Early-stage investment remains active, with strategic positioning in focus: By deal count, Seed and Strategic rounds together accounted for nearly 70%, reflecting investors’ sustained attention to projects with strong innovation potential and ecosystem value. In contrast, Angel and Pre-Seed rounds made up less than 10%, indicating more cautious investor attitudes at the very earliest stages.

Mature projects show a strong capital-magnet effect: In terms of capital distribution, the picture was very different. Series B rounds, though only 9.3% of total deals, captured 45.7% of total funding, becoming the “fundraising champion” of the month. This suggests that capital is concentrating in projects that have already achieved market validation and entered large-scale expansion, with investors increasingly making precise bets. By comparison, while Seed rounds were the most numerous, they only accounted for 19.5% of funding, showing that early-stage capital is spread across frequent small-ticket investments to capture potential breakout projects.

Additionally, unlike July, when capital was concentrated in Series A, August saw funding tilt more heavily toward Series B, signaling that growth-stage investments are shifting to more mature projects. At the same time, several undisclosed rounds explicitly indicated that proceeds would be allocated to acquiring mainstream crypto assets such as ETH and SOL as treasury reserves. While such “financial allocation” financings are not included in conventional statistics, they are emerging as a new model of asset management that bridges Web3 with traditional finance, hinting at a more mature and diversified capital market ahead.

According to data published by Cryptorank on September 16, 2025, the most active investors of the month were concentrated among leading VCs and industry funds. Coinbase Ventures led with 8 deals spanning DeFi, blockchain infrastructure, and CeFi, reflecting the breadth and depth of its ecosystem strategy. HashKey Capital followed with 5 investments, primarily focused on blockchain services and infrastructure in the Asian market, highlighting its regional focus and long-term outlook.

From a sector perspective, DeFi and blockchain infrastructure remained the primary focus areas, appearing in the portfolios of most active investors, underscoring consensus around their long-term value and central role in the ecosystem. Meanwhile, firms such as YZI Labs, Amber Group, and Animoca Brands demonstrated more visible allocations into Chain, Social, and NFT application-layer projects, reflecting differentiated investment strategies—maintaining steady bets on mainstream financial and infrastructure plays while also exploring the next wave of user adoption opportunities.

Overall, the August investment landscape was characterized by a dual pattern: “leading institutions casting wide nets, mid-sized funds pursuing differentiated bets.” The former maintained influence by covering DeFi, CeFi, and infrastructure, while the latter sought breakthroughs in application-layer projects to navigate an environment where fundraising is becoming more selective.

Highlighted Project of the Month

SuperGaming

Overview: SuperGaming is a game studio headquartered in India, focused on developing cross-platform, fair, and socially engaging Web3 games. The company leverages live gaming to attract core players and aims to build a robust ecosystem that supports both players and developers.【3】

On August 6, SuperGaming announced the completion of a $15 million Series B funding round, led by Skycatcher and Steadview Capital, bringing its current valuation to $100 million.【4】

Investors/Angels: Skycatcher, Steadview Capital, A16z Speedrun, Bandai Namco 021 Fund, Neowiz, Polygon Ventures, among others.

Highlights:

- Strong IP and large user base: SuperGaming has launched popular titles such as MaskGun, Battle Stars, and Silly Royale, with over 200 million total installs. Its flagship game, Indus Battle Royale, gained 9 million downloads worldwide shortly after launch, showcasing strong market traction.

- Proprietary technology platform: SuperGaming developed SuperPlatform, a cloud backend solution for building and managing multiplayer games. In partnership with Google Cloud, it provides developers with tools for user dynamics, matchmaking, game progress, data analytics, server scaling, and monetization, underscoring its technical capabilities.

- Dual Web2 + Web3 strategy: By offering both traditional and Web3 games, such as Silly Royale, the company mitigates uncertainty around Web3 adoption while preparing for digital asset ownership use cases. This dual-track model allows SuperGaming to seize opportunities while managing risk.

- Global expansion and top-tier backing: With strong investor support, SuperGaming is positioned for global growth as a leading Indian gaming company. The funding fuels the international rollout of Indus Battle Royale (starting in Latin America) and the enhancement of its technology platform.

Multipli

Overview: Multipli is a real-yield protocol designed to unlock superior risk-adjusted returns for native crypto assets such as Bitcoin, tokenized gold, XRP, and stablecoins, which traditionally generate no yield. The platform leverages real-world asset (RWA) tokenization to bring tangible assets on-chain, creating yield opportunities for traditionally non-yielding assets like stocks and commodities.【5】

On August 28, Multipli announced the completion of a $5 million funding round, bringing its total funding to $21.5 million. The proceeds will be used to expand its suite of institutional-grade yield products for assets like Bitcoin and tokenized gold.【6】

Investors: Pantera Capital, Sequoia Capital, Elevation Capital, among others.

Highlights:

- Transitioning DeFi toward real yield: Multipli is shifting DeFi away from inflationary incentives toward institutional-grade, risk-adjusted real yield. Its API delivers same-day liquidity and transparency, eliminating the lengthy redemption cycles and complex onboarding typical of hedge funds, while enabling tokenized strategies to integrate seamlessly with DeFi protocols.

- Institutional-grade strategies: The platform offers delta-neutral hedge fund strategies designed by firms such as Nomura, Fasanara, and Edge Capital. By tokenizing these strategies, Multipli lowers entry barriers and opens access to a broader investor base.

- Rapid adoption and strong returns: Just weeks after launch, Multipli reached nearly $95 million in TVL, with current levels above $79 million. Investors can earn 6% APY on Bitcoin and 10–15% APY on stablecoins, far outperforming the industry average of under 1%.

- Experienced founding team and partnerships: Founded by early Ethereum contributors and former executives from Coinbase, PayPal, and JPMorgan, Multipli partners with top asset managers to tokenize proven financial strategies—such as positive carry trades, basis arbitrage, and liquidity management—into liquid, composable, and compliant yield products, independent of short-term incentives or mining schemes.

BOB

Overview: BOB (Build on Bitcoin) is a hybrid Layer-2 platform that combines the security of Bitcoin with the flexibility of Ethereum smart contracts. It supports Bitcoin ecosystem features such as Ordinals, Lightning, and Nostr, aiming to enhance Bitcoin’s utility and extend its functionality.【7】

On August 7, BOB announced the completion of a $9.5 million strategic funding round. Since December 2024, the company has completed multiple rounds of strategic financing, raising a total of $21 million.【8】

Investors: Castle Island Ventures, Ledger Cathay Capital, RockawayX, Asymmetric, Hypersphere, IOSG Ventures, Bankless Ventures, Sigil/Zeeprime, CMS, Daedalus, Amber Group, Sats Ventures, and others.

Highlights:

- Through its unique hybrid chain architecture, BOB combines Bitcoin’s security model with Ethereum’s smart contract functionality. Leveraging Layer-2 technology, it significantly improves transaction speed and reduces fees, while maintaining EVM compatibility for interoperability with Ethereum and other ecosystems. This allows developers to deploy smart contracts on the Bitcoin network, introducing complex DeFi applications such as lending and AMMs.

- BOB pioneered the integration of zero-knowledge (ZK) technology into an Optimistic Rollup-based hybrid ZK Rollup, reducing transaction costs and improving efficiency. On the security side, BOB leverages Bitcoin’s PoW model and merged mining to provide Bitcoin-level security, making attacks nearly impossible. It also integrated with Fireblocks to combine its institutional-grade wallet infrastructure with the BOB network, further enhancing security for institutional adoption of Bitcoin DeFi.

- BOB introduced “Fusion Points” and “airdrop” mechanisms to incentivize user participation and network growth. These initiatives not only boost user engagement but also improve platform liquidity and expand the user base, supporting the sustainable development of the ecosystem.

- On its testnet, BOB has already launched native Bitcoin DeFi features and plans to enable trustless BTC deposits/withdrawals through BitVM. With mainnet launch, it will further expand Bitcoin’s role in the DeFi space.

HoneyCoin

Overview: HoneyCoin is a fintech platform that allows users to manage both fiat and digital currencies through a unified interface. It supports multiple payment methods, including mobile money systems, bank transfers, and cryptocurrencies, making it easier to conduct cross-border transactions and local payments.【9】

On August 12, HoneyCoin announced the completion of a $4.9 million funding round, led by Flourish Ventures. The funds will be used to scale operations, expand its product suite, and strengthen the leadership team.【10】

Investors/Angel Backers: Flourish Ventures, Visa Ventures, Lava, TLCom, Antler, Musha Ventures, 4DX Ventures, Stellar Development Foundation, James Waugh (Fire Eyes), Vasily Shapovalov (Co-founder of Lido), among others.

Highlights:

- HoneyCoin focuses on solving inefficiencies in global financial settlement, particularly for enterprises in emerging markets. Through its stablecoin liquidity engine, the platform provides businesses with unified tools for collections, treasury management, settlement, and FX services—enabling instant or same-day clearing compared to the traditional 4–7 business day timeline.

- HoneyCoin’s monthly transaction volume has exceeded $150 million, serving over 350 enterprise clients and hundreds of thousands of users. Its flagship app, Peer, scaled from processing a few hundred dollars to over $100 million, showcasing strong demand and scalability.

- HoneyCoin has expanded into 45+ countries/regions and obtained licenses/certifications (including PCI-DSS Level 1 compliance) in 15 African markets as well as major jurisdictions in Europe and the U.S. Its FXHub supports real-time trading of 49 currencies, helping CFOs and finance teams optimize global treasury management. The company has partnered with MoneyGram, UBA Bank, and Stripe, while also being adopted by fast-growing enterprises such as Cedar Money, TerraPay, and Jiji.

Perle

Overview: Perle is a platform designed for managing AI training data. Built around a workflow that incorporates human experts into the data-labeling process, it supports multimodal AI models across text, image, audio, and video.【11】

On August 7, Perle announced the completion of a $9 million seed round led by Framework Ventures, bringing its total funding to $17.5 million.【12】

Investors: Framework Ventures, among others.

Highlights:

- Perle does not directly compete with model developers like OpenAI. Instead, it positions itself as a “data energy provider.” Its platform, Perle Labs, focuses on collecting high-quality human feedback data—a scarce and valuable resource that strengthens AI model training.

- Each piece of feedback data is recorded on the blockchain, including its source, contributor, and quality, ensuring transparency and traceability. Contributors are rewarded with tokens or on-chain assets, turning data production into a sustainable economic activity and addressing the issues of trust and lack of incentives in the traditional AI industry.

- Perle Labs is open to all AI development teams, not tied to a single ecosystem, and supports multiple AI use cases. The platform includes built-in tools for data collection, quality control, evaluation, and rapid iteration. It also supports reinforcement learning with human feedback (RLHF), helping various models improve robustness and safety.

- By leveraging a distributed network of professional annotators for data validation, combined with blockchain-based records and incentive mechanisms, Perle reduces bias, enhances model performance, and builds a trustworthy, efficient infrastructure for human feedback data in AI training.

Conclusion

In August 2025, total Web3 funding reached $2.05 billion across 112 deals. Although the overall scale declined, structural shifts clearly indicate the industry is entering a more mature and rational phase: capital is no longer concentrated in “hype-driven mega-bets” but is moving toward “steady, diversified allocations.” CeFi once again demonstrated strong capital absorption, infrastructure and mid-sized growth projects received consistent support, while application-layer projects faced accelerated elimination.

From a funding-stage perspective, the activity in seed and strategic rounds highlights that innovation and ecosystem synergies remain key focuses for investors; meanwhile, the dominance of Series B deals shows that capital is flowing toward market-validated, more mature projects. At the same time, the penetration of traditional capital instruments (IPOs, convertible bonds) and the trend of listed companies adding crypto assets to their corporate treasuries signal the deepening integration of Web3 with mainstream financial markets.

Key funding cases further validate this trajectory: SuperGaming showcased the migration potential of Web2 users into blockchain via its dual Web2+Web3 model; Multipli drove DeFi’s shift toward “real yield,” replacing inflationary tokenomics with institutional-grade strategies; BOB enhanced Bitcoin’s utility through hybrid chain technology and smart contract functionality; HoneyCoin and Perle demonstrated Web3’s real-world value in inclusive finance and AI training data, respectively.

Overall, this month’s funding signals that Web3 is moving from speculation to application, from concept to maturity—ushering in a steady, diversified, and sustainable growth phase.

Reference:

- Cryptorank , https://cryptorank.io/funding-analytics

- Cryptorank, https://cryptorank.io/funding-rounds

- SuperGaming, https://www.supergaming.com/

- Tech in Asia, https://www.techinasia.com/news/a16z-polygon-back-15m-series-b-for-indian-gaming-studio

- Multipli, https://multipli.fi/

- Chainwire, https://chainwire.org/2025/08/28/multipli-hits-21-5m-in-total-funding-as-it-expands-institutional-yield-for-crypto-rwa-assets/?mfk=HZ3EsEJFHaL5bDGEP6TtWHZFEYAnzfCtUK%2BvwySqTsMbN46poLI3yHvzsvDkS1D6wPhF7%2F0yBYKVKYkhLxdluzsJ9lHLqP9YH0dkxWz%2FAa3KKA%3D%3D

- BOB, https://www.gobob.xyz/

- X, https://x.com/build_on_bob/status/1953369142821830818

- HoneyCoin, https://honeycoin.app/

- HoneyCoin, https://blog.honeycoin.app/honeycoin-raises-49m

- Perle, https://www.perle.ai/

- The Block, https://www.theblock.co/post/366058/framework-ventures-leads-9-million-seed-round-for-web3-powered-ai-project-perle

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.

Share

Related Articles

Gate Research: 2024 Cryptocurrency Market Review and 2025 Trend Forecast

Gate Research: BTC Breaks $100K Milestone, November Crypto Trading Volume Exceeds $10 Trillion For First Time

Gate Research-A Study on the Correlation Between Memecoin and Bitcoin Prices

Altseason 2025: Narrative Rotation and Capital Restructuring in an Atypical Bull Market

Detailed Analysis of the FIT21 "Financial Innovation and Technology for the 21st Century Act"